How to check your credit report for signs of identity theft is one of the most important steps you can take to protect your finances and catch fraud before it gets worse. Identity thieves often leave clues behind, such as unauthorized accounts, fraudulent inquiries, incorrect personal information, and suspicious activity that appears on your credit report long before victims realize something is wrong. In this guide, you’ll learn how to review your credit reports, identify common identity theft warning signs, and take action quickly if you discover evidence of fraud. By following these steps, you can better protect your credit, your personal information, and your financial future.

If you’re worried that your personal information has already been compromised, learn the most common warning signs in our guide on How to Know If Someone Stole Your Identity.

Table of Contents

What Is Identity Theft and Why Your Credit Report Matters

Identity theft occurs when someone uses your personal information—such as your Social Security number, date of birth, bank account details, or credit card information—without your permission to commit fraud. Criminals may open new credit accounts, apply for loans, make purchases, or even create utility accounts in your name.

Unfortunately, many victims do not discover the problem until significant financial damage has already occurred. That’s why learning how to check your credit report for signs of identity theft is one of the most important steps you can take to protect your finances.

Your credit report acts as a financial history record. It contains information about your credit accounts, payment history, credit inquiries, addresses, and other identifying details. Because fraudulent activity often appears on a credit report before victims receive alerts or collection notices, regularly reviewing your report can help you detect identity theft early.

When reviewing your report, watch for common signs of identity theft, including:

- Credit accounts you do not recognize

- Unauthorized credit inquiries

- Incorrect personal information

- Unexpected changes to your address

- Collection accounts that are unfamiliar

- Loans or credit cards you never applied for

These are often the earliest identity theft warning signs that criminals may be using your information.

Many people assume that checking their bank account is enough, but fraudulent accounts on a credit report can remain unnoticed for months if you are not actively monitoring your credit files. This is why financial experts recommend reviewing your reports regularly and using identity monitoring services that can alert you to suspicious activity.

In this guide, you’ll learn how to check your credit report for signs of identity theft, identify unauthorized accounts on your credit report, recognize suspicious activity, and take immediate action if you discover evidence of fraud.

For additional information about credit reports and consumer rights, you can visit:

- AnnualCreditReport.com

- Federal Trade Commission Identity Theft Resources

- Consumer Financial Protection Bureau Credit Report Guide

The sooner you learn how to check your credit report for signs of identity theft, the better your chances of stopping fraud before it causes serious financial harm.

To better understand how criminals obtain your information in the first place, read our guide on How Identity Theft Happens.

How to Check Your Credit Report for Signs of Identity Theft

Learning how to check your credit report for signs of identity theft can help you discover fraudulent activity before it causes major financial damage. Many identity theft victims don’t realize their information has been compromised until they are denied credit, receive collection notices, or notice unfamiliar accounts on their reports.

The good news is that reviewing your credit report is a straightforward process that can reveal many of the most common signs of identity theft.

Step 1: Obtain Your Credit Reports

Start by requesting your credit reports from all three major credit bureaus:

- Experian

- Equifax

- TransUnion

Reviewing reports from all three bureaus is important because fraudulent accounts on a credit report may appear on one report before appearing on the others.

Step 2: Verify Your Personal Information

The first section of your report contains identifying information such as:

- Full name

- Current and previous addresses

- Social Security number (partially displayed)

- Date of birth

- Employment history

Look for:

- Addresses you do not recognize

- Employers you’ve never worked for

- Name variations you haven’t used

- Incorrect contact information

Criminals often update account information to gain access to credit accounts, making these changes potential identity theft warning signs.

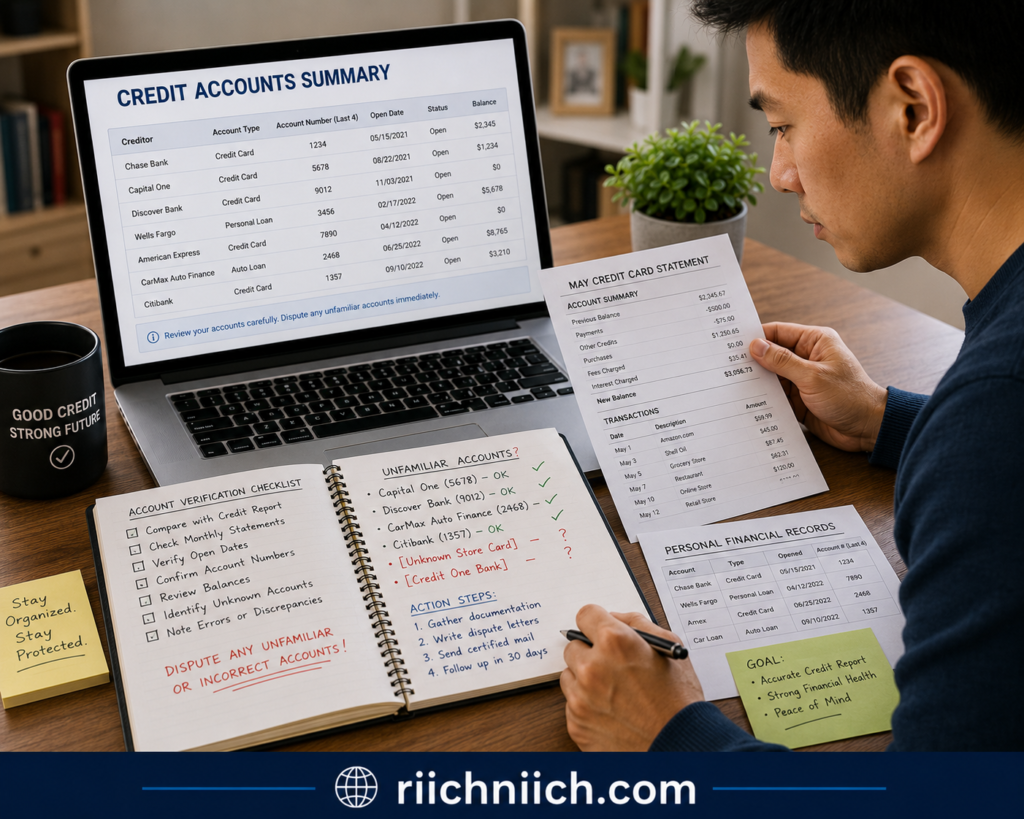

Step 3: Review All Open Credit Accounts

One of the most important steps in how to check your credit report for signs of identity theft is examining every account listed.

Pay close attention to:

- Credit cards

- Personal loans

- Auto loans

- Mortgages

- Retail store credit accounts

Ask yourself:

- Did I open this account?

- Do I recognize the lender?

- Are the balances accurate?

Unauthorized accounts on a credit report are among the strongest indicators that someone may be using your identity.

Step 4: Check Credit Inquiries

Credit inquiries show when lenders have reviewed your credit file.

There are two types:

- Soft inquiries

- Hard inquiries

Focus on hard inquiries because they usually occur when someone applies for credit.

If you see inquiries from companies you never contacted, it may indicate attempted fraud or new account applications submitted without your permission.

Step 5: Look for Collection Accounts

Collection accounts can be a major red flag.

Review your report carefully for:

- Medical collections

- Utility collections

- Credit card collections

- Debt collection entries

Many identity theft victims first discover fraud after seeing unpaid debts linked to accounts they never opened.

These entries often indicate that fraudulent accounts have already progressed into delinquency.

Step 6: Watch for Sudden Credit Score Changes

A significant drop in your credit score can signal identity theft.

Unexpected decreases may result from:

- New accounts

- High balances

- Missed payments

- Collection activity

While a lower score does not automatically mean fraud, it should prompt a closer review of your report.

Step 7: Document Any Suspicious Activity

If you identify suspicious activity on your credit report, create a record immediately.

Save:

- Screenshots

- Account numbers

- Inquiry details

- Collection information

- Dates of discovery

Keeping detailed records can simplify the dispute process and support identity theft investigations.

Checking your credit report regularly is essential, but it only shows problems after they appear.

👉 If you want real-time alerts for suspicious activity, new credit accounts, and potential identity theft, consider using a trusted identity theft protection service like Aura before fraud has a chance to spread.

Consider Ongoing Monitoring

Even if your report appears clean today, identity theft can occur at any time. Many consumers choose identity monitoring services that provide alerts for:

- New account activity

- Credit inquiries

- Changes to personal information

- Suspicious financial activity

These services can help detect fraudulent accounts on a credit report before the damage becomes severe.

By consistently following these steps, you’ll know how to check your credit report for signs of identity theft and improve your ability to detect suspicious activity, unauthorized accounts, and credit report fraud before they escalate into larger financial problems.

Regular monitoring remains one of the most effective ways to identify identity theft warning signs early and protect your financial future.

Where to Get Free Copies of Your Credit Reports

Before you can learn how to check your credit report for signs of identity theft, you first need access to your credit reports. Fortunately, federal law allows consumers to obtain free copies of their credit reports from the three major credit bureaus.

Regularly reviewing your reports is one of the best ways to detect fraudulent accounts on a credit report, identify unauthorized credit inquiries, and uncover suspicious activity before it causes serious financial harm.

AnnualCreditReport.com

The safest and most widely recommended place to obtain free credit reports is:

This website is authorized by federal law and provides access to reports from:

- Experian

- Equifax

- TransUnion

Requesting reports through this official source helps ensure you are viewing accurate information directly from the credit bureaus.

Request Reports From All Three Credit Bureaus

Many consumers only review one report, but identity theft can appear on a single bureau before it appears elsewhere.

To effectively practice how to check your credit report for signs of identity theft, review all three reports and compare them for:

- Unauthorized accounts on a credit report

- Incorrect personal information

- Fraudulent inquiries

- Collection accounts you do not recognize

- Suspicious financial activity

Checking all three reports provides a more complete picture of your credit history.

What Information You’ll Need

When requesting your reports, be prepared to verify your identity using information such as:

- Full legal name

- Date of birth

- Social Security number

- Current address

- Previous address information

These verification steps help prevent criminals from accessing your credit information.

Download and Save Your Reports

Once your reports become available, download and save copies for future reference.

This allows you to:

- Compare future reports

- Track changes over time

- Document suspicious activity

- Support fraud investigations if necessary

Maintaining historical records can make it easier to spot identity theft warning signs that might otherwise go unnoticed.

How Often Should You Check Your Credit Reports?

Many experts recommend reviewing your reports several times throughout the year.

You may want to check more frequently if:

- You’ve experienced a data breach

- Your information was exposed online

- You received fraud alerts

- You notice unusual financial activity

- You suspect identity theft

The earlier you discover fraudulent accounts on a credit report, the easier it is to limit the damage.

Consider Credit and Identity Monitoring

While manually reviewing reports is essential, monitoring services can provide additional protection by alerting you to:

- New credit applications

- Hard inquiries

- Changes to personal information

- Newly opened accounts

- Suspicious financial activity

These alerts can help consumers detect identity theft warning signs sooner and take action before fraud spreads.

Common Mistakes to Avoid

When obtaining your reports, avoid these common mistakes:

- Reviewing only one credit bureau

- Ignoring unfamiliar inquiries

- Overlooking address changes

- Failing to save copies for comparison

- Waiting until a problem occurs before checking

Being proactive is one of the most effective ways to learn how to check your credit report for signs of identity theft and protect your financial future.

Obtaining your reports is the first step toward identifying unauthorized accounts on a credit report, detecting credit report fraud, and protecting yourself from identity theft before it becomes a larger financial problem.

10 Warning Signs of Identity Theft on Your Credit Report

One of the most effective ways to learn how to check your credit report for signs of identity theft is knowing exactly what warning signs to look for. Criminals often leave clues behind long before victims realize their identities have been compromised.

By regularly reviewing your credit reports, you can spot suspicious activity, identify fraudulent accounts on a credit report, and take action before the damage becomes more severe.

1. Credit Accounts You Don’t Recognize

If you discover a credit card, loan, or line of credit that you never opened, this is one of the strongest indicators of identity theft.

Unauthorized accounts on a credit report often mean a criminal successfully used your personal information to obtain credit.

2. Hard Inquiries You Didn’t Authorize

When someone applies for credit, lenders typically perform a hard inquiry.

If you notice hard inquiries from companies you’ve never contacted, it could indicate attempted fraud or account applications submitted in your name.

These inquiries are often among the earliest identity theft warning signs.

3. Incorrect Addresses Appearing on Your Report

Identity thieves frequently update account information to gain access to financial accounts.

Watch for:

- Addresses you never lived at

- Mailing addresses you don’t recognize

- Sudden address changes

Incorrect addresses can signal suspicious activity linked to your identity.

4. Unknown Employers Listed

Credit reports sometimes include employment information.

If you see employers you’ve never worked for, it may indicate someone else is using your personal information to apply for credit or employment.

5. Collection Accounts You Don’t Recognize

Collection accounts are serious red flags.

Many victims discover identity theft only after seeing unpaid debts associated with unfamiliar accounts.

If a collection agency appears on your report and you don’t recognize the debt, investigate immediately.

6. Unexpected Drops in Your Credit Score

A sudden decrease in your credit score can indicate:

- New fraudulent accounts

- High balances

- Missed payments

- Collection activity

Although credit score changes can occur for legitimate reasons, unexpected declines should never be ignored.

7. Personal Information Changes You Didn’t Make

Review your identifying information carefully.

Look for:

- Name variations

- Incorrect phone numbers

- Unknown email addresses

- Changed contact details

Identity thieves often alter account information to maintain control over stolen accounts.

8. New Loans You Never Requested

Fraudsters commonly use stolen information to obtain:

- Personal loans

- Auto loans

- Retail financing

- Installment loans

Any unfamiliar loan listed on your report should be investigated immediately.

9. Duplicate Accounts With Different Information

Sometimes criminals create variations of existing accounts.

You may notice:

- Similar account numbers

- Duplicate lender entries

- Slightly altered personal information

These unusual entries can indicate credit report fraud and identity theft.

10. Accounts Showing Late Payments You Didn’t Miss

If your report shows missed payments on accounts you don’t recognize, this could indicate fraudulent accounts on a credit report.

Many identity theft victims first notice problems after seeing late payments connected to accounts they never opened.

Why These Warning Signs Matter

The sooner you identify these issues, the easier it becomes to stop fraud.

Learning how to check your credit report for signs of identity theft allows you to:

- Detect unauthorized accounts on a credit report

- Identify suspicious financial activity

- Catch fraudulent inquiries early

- Protect your credit score

- Reduce long-term financial damage

Many consumers choose identity monitoring services to receive alerts when new accounts, inquiries, or changes appear on their credit files. Early detection can make a significant difference when recovering from identity theft.

Take Action Immediately

If you discover any of these warning signs:

- Document the suspicious information.

- Contact the affected lender.

- Dispute inaccurate information with the credit bureau.

- Consider placing a fraud alert.

- Consider freezing your credit files.

The faster you respond, the better your chances of limiting financial losses and preventing additional fraud.

Understanding these warning signs is a critical part of how to check your credit report for signs of identity theft and can help you identify fraud before it turns into a much larger financial problem.

Want a more complete checklist? Read our article on 13 Warning Signs Someone Stole Your Identity to learn additional red flags to watch for.

How to Review Personal Information for Suspicious Changes

When learning how to check your credit report for signs of identity theft, many people focus only on credit accounts and inquiries. However, one of the earliest signs of fraud often appears in the personal information section of your credit report.

Identity thieves frequently change personal details to gain control of accounts, redirect communications, or support fraudulent credit applications. Carefully reviewing this section can help you detect suspicious activity before it leads to larger financial problems.

What Personal Information Appears on a Credit Report?

Your credit report may include information such as:

- Full legal name

- Name variations

- Current address

- Previous addresses

- Date of birth

- Social Security number (partially masked)

- Phone numbers

- Employment history

While some minor inaccuracies can occur naturally, unfamiliar information should always be investigated.

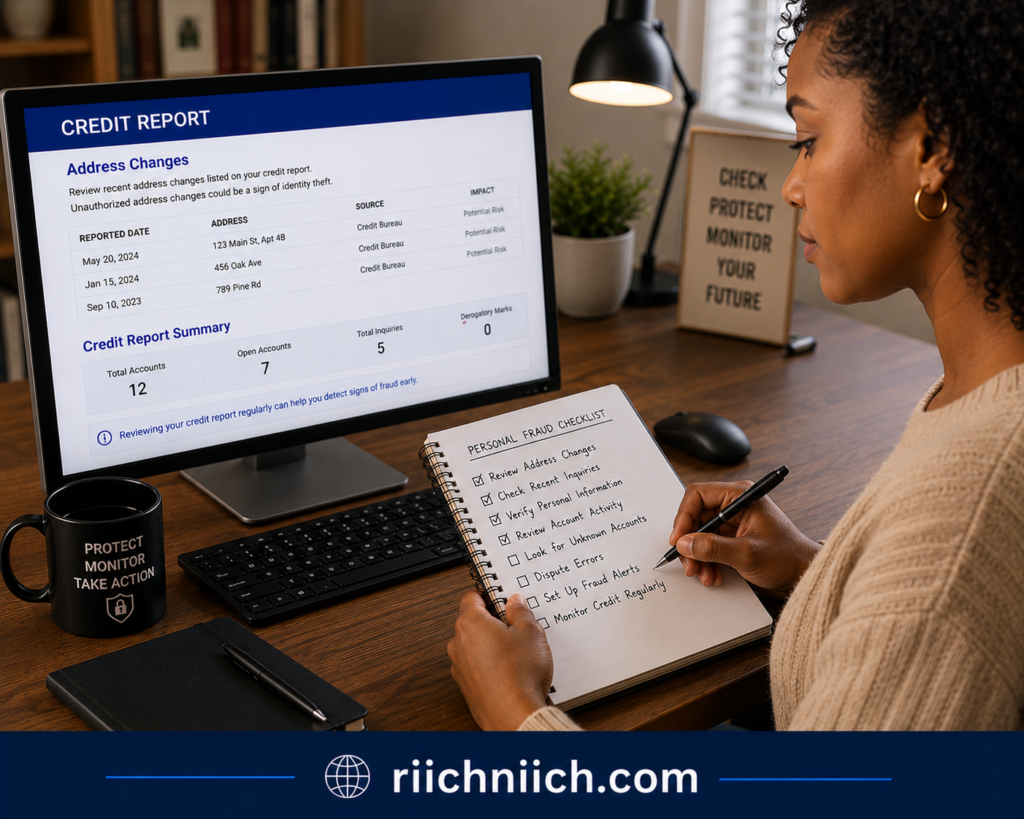

Check for Unknown Addresses

One of the most common identity theft warning signs is an address you do not recognize.

Look for:

- Addresses where you have never lived

- Recently added addresses

- Mailing addresses you didn’t authorize

- Locations in unfamiliar cities or states

Criminals sometimes add new addresses to support fraudulent account applications or to redirect important financial documents.

If you notice an unfamiliar address, it may indicate unauthorized activity connected to your identity.

Review Name Variations Carefully

Credit reports often contain variations of your name.

For example:

- Middle initials

- Maiden names

- Common abbreviations

However, unusual name variations may signal identity theft.

Watch for:

- Misspelled names

- Different middle names

- Completely unfamiliar aliases

- Alternate last names you have never used

These discrepancies can sometimes appear when someone uses your personal information to apply for credit.

Verify Employment Information

Employment history can occasionally reveal signs of fraud.

Review employer listings for:

- Companies you’ve never worked for

- Incorrect job titles

- Unknown employment records

While employment data isn’t always perfectly updated, unfamiliar employers may indicate someone is using your information in credit or employment applications.

Examine Contact Information

Identity thieves may attempt to gain control of accounts by changing contact details.

Review any listed:

- Phone numbers

- Email addresses

- Mailing information

If you discover contact information you do not recognize, investigate immediately.

Unauthorized changes can make it easier for criminals to intercept account notifications and security alerts.

Compare Information Across All Three Credit Reports

One important part of how to check your credit report for signs of identity theft is reviewing reports from:

- Experian

- Equifax

- TransUnion

A suspicious address or personal detail may appear on one report before appearing on the others.

Comparing all three reports improves your chances of identifying fraudulent activity early.

Keep Records of Any Discrepancies

If you discover suspicious information, document everything.

Save:

- Screenshots

- Report copies

- Dates of discovery

- Notes about inaccuracies

Maintaining detailed records can help when disputing inaccurate information with credit bureaus or lenders.

Why Personal Information Changes Matter

Many consumers focus only on fraudulent accounts on a credit report, but suspicious personal information changes often occur before new accounts appear.

These changes may indicate:

- Attempted identity theft

- Account takeover fraud

- Synthetic identity fraud

- Unauthorized credit applications

Detecting these warning signs early can help prevent more serious financial damage.

Consider Ongoing Identity Monitoring

Regular credit report reviews are important, but identity monitoring services can provide additional protection by alerting you to:

- Personal information changes

- New credit applications

- Account activity

- Suspicious financial events

Early notifications can help you respond quickly if criminals attempt to misuse your information.

Reviewing personal details may seem simple, but it is a critical step in how to check your credit report for signs of identity theft. Identifying suspicious changes early can help stop fraud before criminals open accounts, damage your credit, or create long-term financial headaches.

How to Spot Unauthorized Credit Accounts

One of the most important parts of how to check your credit report for signs of identity theft is identifying credit accounts that do not belong to you. Unauthorized accounts on a credit report are among the clearest indicators that someone may be using your personal information to obtain credit, loans, or financial services.

The sooner you identify fraudulent accounts on a credit report, the easier it becomes to stop additional fraud and limit damage to your credit score.

Review Every Account Individually

Many people quickly scan their credit reports and focus only on their credit score. However, effective fraud detection requires a closer review of every listed account.

Check each account for:

- Lender name

- Account type

- Date opened

- Current balance

- Credit limit

- Payment history

Ask yourself:

- Did I open this account?

- Do I recognize this lender?

- Does the opening date seem accurate?

- Is the balance consistent with my records?

Even one unfamiliar account deserves immediate attention.

Watch for Accounts Opened Recently

Identity thieves often move quickly after obtaining personal information.

Pay special attention to accounts that were:

- Opened within the past few months

- Established during a recent data breach

- Created after suspicious emails or phishing attempts

New accounts are often among the earliest identity theft warning signs visible on a credit report.

Look Beyond Credit Cards

Many consumers only focus on credit cards, but criminals may open several different types of accounts.

Review reports for:

- Personal loans

- Auto loans

- Retail financing accounts

- Store credit cards

- Buy-now-pay-later accounts

- Lines of credit

Any unfamiliar account could indicate suspicious financial activity linked to identity theft.

Check Account Status Carefully

Fraudulent accounts on a credit report may appear in different statuses.

Watch for accounts marked as:

- Open

- Active

- Charged off

- Delinquent

- In collections

Even closed accounts should be reviewed because identity thieves sometimes open accounts, use them briefly, and abandon them before victims discover the fraud.

Compare Reports From All Three Credit Bureaus

A key step in how to check your credit report for signs of identity theft is reviewing reports from all three major credit bureaus.

These include:

- Experian

- Equifax

- TransUnion

An unauthorized account on a credit report may appear on one bureau’s report before appearing on the others.

Comparing reports helps uncover discrepancies that could otherwise be missed.

Review Joint and Authorized User Accounts

Sometimes consumers mistake legitimate shared accounts for fraud.

Before reporting an account as unauthorized, determine whether:

- You were added as an authorized user

- You previously held a joint account

- The account belongs to a spouse or family member

If the account remains unfamiliar after verification, further investigation is warranted.

Investigate Small Accounts Too

Identity thieves don’t always start with large loans.

Some criminals intentionally open:

- Small retail accounts

- Low-limit credit cards

- Financing accounts with modest balances

These accounts may go unnoticed for months if consumers focus only on major financial obligations.

Every account should be reviewed regardless of size.

What to Do If You Find an Unauthorized Account

If you discover an account you did not open:

- Document the account information.

- Contact the lender immediately.

- Request fraud investigation procedures.

- File disputes with the credit bureaus.

- Consider placing a fraud alert.

- Consider freezing your credit files.

Quick action can help prevent additional fraudulent activity and minimize credit damage.

Consider Ongoing Monitoring

Many consumers use identity monitoring services to help detect:

- New account openings

- Credit report changes

- Unauthorized inquiries

- Suspicious financial activity

Monitoring services can provide alerts before fraudulent accounts on a credit report cause significant financial harm.

Learning how to check your credit report for signs of identity theft includes more than simply reviewing your credit score. Carefully examining every account on your report can help you identify unauthorized accounts on a credit report, detect suspicious activity early, and protect your financial future before identity theft becomes a larger problem.

Finding even one unfamiliar account can be a sign that your personal information has already been compromised.

👉 An identity theft protection service like Aura can monitor your credit and alert you to new account activity much sooner than waiting to discover it during your next credit report review.

How to Identify Fraudulent Inquiries on Your Credit Report

When learning how to check your credit report for signs of identity theft, many people focus on unfamiliar accounts but overlook credit inquiries. However, fraudulent inquiries are often one of the earliest warning signs that someone is attempting to use your personal information to obtain credit.

Identity thieves frequently apply for credit cards, loans, and financing using stolen information. Even if an application is denied, the inquiry may still appear on your credit report and provide an important clue that fraud is occurring.

What Are Credit Inquiries?

A credit inquiry occurs when someone reviews your credit file.

There are two primary types:

Soft Inquiries

Soft inquiries generally occur when:

- You check your own credit

- Companies send pre-approved offers

- Existing lenders review your account

Soft inquiries typically do not affect your credit score.

Hard Inquiries

Hard inquiries usually occur when someone applies for:

- Credit cards

- Auto loans

- Mortgages

- Personal loans

- Retail financing

Hard inquiries are the ones you should examine closely when performing how to check your credit report for signs of identity theft.

Why Fraudulent Inquiries Matter

Fraudulent inquiries can indicate that someone is actively attempting to open accounts using your identity.

Even if the application is denied, criminals may continue submitting applications elsewhere.

A single unauthorized inquiry may not seem serious, but it can be one of the earliest identity theft warning signs on your credit report.

How to Review Your Inquiry Section

Locate the inquiry section on each credit report from:

- Experian

- Equifax

- TransUnion

Review:

- Company names

- Dates of inquiries

- Types of inquiries

Ask yourself:

- Did I apply for credit with this company?

- Do I recognize the lender?

- Does the inquiry date match an application I submitted?

Any unfamiliar inquiry deserves further investigation.

Watch for Unknown Lenders

One of the most common signs of suspicious activity is seeing inquiries from lenders you have never contacted.

Examples may include:

- Credit card issuers

- Auto finance companies

- Personal loan providers

- Retail financing companies

If you have no record of applying for credit with a company, the inquiry could indicate attempted fraud.

Pay Attention to Multiple Inquiries

Several hard inquiries appearing within a short period can be a warning sign.

Identity thieves often submit multiple applications quickly in an attempt to secure credit before detection.

Look for:

- Multiple inquiries within days

- Applications from similar lenders

- Several inquiries from unfamiliar companies

Clusters of inquiries may indicate ongoing identity theft activity.

Verify Legitimate Applications

Not every unfamiliar inquiry is fraudulent.

Sometimes inquiries appear because of:

- Financing applications

- Apartment rental screenings

- Utility account requests

- Insurance applications

Before assuming fraud, verify whether you recently authorized any activity that required a credit check.

What to Do If You Find a Fraudulent Inquiry

If you identify an inquiry you did not authorize:

- Document the inquiry details.

- Contact the lender listed.

- Ask whether an application was submitted.

- Request fraud investigation procedures.

- File disputes with the credit bureaus if appropriate.

- Consider placing a fraud alert on your credit file.

- Consider freezing your credit files.

Taking action quickly may help prevent unauthorized accounts from being opened.

Monitor for Additional Activity

Fraudulent inquiries often occur before unauthorized accounts appear on a credit report.

After discovering a suspicious inquiry, continue monitoring your reports for:

- New credit accounts

- Additional inquiries

- Address changes

- Collection accounts

- Credit score fluctuations

Early detection is one of the most effective ways to limit financial damage.

Consider Identity Monitoring Services

Many identity monitoring services provide alerts when:

- New inquiries appear

- Credit files change

- New accounts are opened

- Personal information is modified

These alerts can help consumers identify suspicious financial activity before identity theft escalates.

Understanding inquiry activity is a critical part of how to check your credit report for signs of identity theft. By identifying fraudulent inquiries early, you can detect unauthorized credit applications, prevent fraudulent accounts on a credit report, and take action before identity thieves cause more extensive financial harm.

How to Check for Incorrect Addresses, Employers, and Contact Information

When people learn how to check your credit report for signs of identity theft, they often focus on credit accounts and inquiries. However, incorrect addresses, employers, and contact information can be some of the earliest indicators that someone is using your personal information.

Identity thieves frequently modify personal details to support fraudulent credit applications, gain access to financial accounts, or redirect important communications. Reviewing this information carefully can help you uncover suspicious activity before unauthorized accounts on a credit report begin to appear.

Why Personal Information Changes Can Signal Identity Theft

Your credit report contains identifying details that lenders use to verify your identity.

These details may include:

- Current address

- Previous addresses

- Phone numbers

- Employment history

- Name variations

When criminals use stolen information, they often introduce new personal details into your credit file.

As a result, unfamiliar information can be one of the first identity theft warning signs visible on your report.

Review Every Address Listed

Start by carefully examining all addresses that appear on your credit report.

Look for:

- Addresses where you have never lived

- Recently added addresses you don’t recognize

- Addresses in unfamiliar cities or states

- Incorrect mailing addresses

Identity thieves sometimes add addresses when applying for loans, credit cards, or other financial products.

Even if no unauthorized accounts on a credit report are visible yet, a suspicious address may indicate attempted fraud.

Verify Previous Address History

It’s normal for your report to contain legitimate former addresses.

However, you should still verify that each address belongs to you.

Pay close attention to:

- Addresses from different states

- Apartment numbers you don’t recognize

- Recent address additions

Unexpected address changes can signal suspicious financial activity linked to your identity.

Examine Employment Information Carefully

Employment records may also reveal potential fraud.

Review the employers listed on your report and ask yourself:

- Have I worked for this company?

- Is the employment period accurate?

- Do I recognize the employer name?

While employment data is not always perfectly updated, unfamiliar employers should never be ignored.

Criminals sometimes use stolen identities when applying for jobs, loans, or other services that require employment verification.

Check Phone Numbers and Contact Information

Some credit reports may include contact information associated with your credit file.

Review:

- Phone numbers

- Mailing information

- Other identifying details

Watch for:

- Phone numbers you never used

- Contact information from another state

- Recently added details that seem unfamiliar

Changes to contact information may indicate attempts to redirect account communications or verification requests.

Look for Name Variations

Minor name variations are often harmless, but some changes deserve closer inspection.

Examples include:

- Misspelled names

- Incorrect middle names

- Unrecognized aliases

- Different last names

Unusual name variations may indicate someone is using your information alongside slightly altered personal details.

Compare Information Across All Three Credit Reports

A key part of how to check your credit report for signs of identity theft is reviewing reports from:

- Experian

- Equifax

- TransUnion

An incorrect address or unfamiliar employer may appear on one report before appearing on the others.

Comparing all three reports can help identify discrepancies that might otherwise go unnoticed.

Document Any Suspicious Information

If you find information that appears inaccurate:

- Save copies of the reports.

- Record the details.

- Note when you discovered the issue.

- Keep screenshots or printed copies.

Proper documentation can help support disputes and fraud investigations later.

Why These Small Details Matter

Many identity theft victims overlook incorrect personal information because it seems less serious than a fraudulent account.

However, suspicious personal details often appear before:

- New credit accounts

- Fraudulent inquiries

- Collection accounts

- Credit score damage

Catching these warning signs early may prevent larger financial problems.

Consider Ongoing Monitoring

Identity monitoring services can alert you when:

- Personal information changes

- New accounts are opened

- Credit inquiries occur

- Suspicious activity is detected

These alerts may help consumers identify credit report fraud before unauthorized accounts on a credit report cause significant damage.

Reviewing addresses, employers, and contact information is an important part of how to check your credit report for signs of identity theft. These details may seem minor, but they often provide some of the earliest clues that your identity is being misused, giving you an opportunity to act before more serious fraud occurs.

What to Do If You Find Signs of Identity Theft

Learning how to check your credit report for signs of identity theft is only the first step. If you discover suspicious activity, unauthorized accounts on a credit report, fraudulent inquiries, or incorrect personal information, taking immediate action can help prevent further financial damage.

The sooner you respond, the better your chances of stopping identity thieves before they open additional accounts, increase debt, or severely impact your credit score.

Step 1: Document Everything

Before making phone calls or filing disputes, gather evidence of the suspicious activity.

Save:

- Copies of your credit reports

- Screenshots of fraudulent accounts

- Inquiry records

- Collection notices

- Account statements

- Any related emails or letters

Maintaining detailed records can simplify the recovery process and support future disputes.

Step 2: Contact the Affected Lenders

If you find accounts you did not open, contact the lender immediately.

Ask to:

- Report the account as fraudulent

- Freeze further activity

- Begin a fraud investigation

- Request written confirmation

Many financial institutions have dedicated fraud departments that can assist identity theft victims.

Step 3: File a Report at IdentityTheft.gov

The Federal Trade Commission provides an official recovery process through:

This resource helps victims:

- Create a recovery plan

- Generate identity theft reports

- Document fraud

- Understand next steps

An official report may also help support disputes with lenders and credit bureaus.

Step 4: Dispute Fraudulent Information With Credit Bureaus

If fraudulent accounts on a credit report appear, file disputes with:

- Experian

- Equifax

- TransUnion

Provide:

- Copies of supporting documentation

- Fraud reports

- Account information

- Written explanations

Credit bureaus are responsible for investigating disputed information and correcting inaccuracies when appropriate.

Step 5: Consider Placing a Fraud Alert

A fraud alert notifies lenders that they should verify your identity before approving new credit applications.

Fraud alerts can:

- Add an extra layer of protection

- Help prevent additional fraudulent accounts

- Reduce the risk of further identity theft

This is often a smart step after discovering suspicious financial activity.

Step 6: Freeze Your Credit Files

Many experts recommend freezing your credit after discovering identity theft.

A credit freeze can:

- Restrict access to your credit reports

- Make it harder for criminals to open new accounts

- Reduce future fraud risk

Freezing your credit is one of the strongest defenses against continued misuse of your personal information.

Step 7: Monitor Existing Financial Accounts

Identity thieves often target more than one account.

Review:

- Bank accounts

- Credit cards

- Investment accounts

- Retirement accounts

- Online payment services

Watch closely for:

- Unauthorized transactions

- Login attempts

- Account changes

- New account alerts

Early detection can significantly reduce financial losses.

Step 8: Change Important Passwords

If your information was exposed through a data breach or phishing attack, update passwords for:

- Email accounts

- Banking accounts

- Credit card portals

- Shopping websites

- Financial apps

Strong, unique passwords can help prevent additional account compromise.

Step 9: Continue Monitoring Your Credit Reports

Even after disputes are filed, continue reviewing your credit reports regularly.

Identity thieves sometimes:

- Open new accounts later

- Reapply using stolen information

- Attempt additional fraud after initial detection

Ongoing monitoring remains an essential part of how to check your credit report for signs of identity theft and protecting your financial future.

Consider Identity Theft Protection Services

Many consumers choose identity theft protection services after discovering fraud because these services can help monitor:

- Credit activity

- New account openings

- Personal information changes

- Dark web exposure

- Identity theft warning signs

These tools may provide earlier alerts and additional recovery support if future incidents occur.

Don’t Delay Action

One of the biggest mistakes identity theft victims make is assuming a suspicious account or inquiry is a simple error.

If you discover:

- Unauthorized accounts on a credit report

- Fraudulent inquiries

- Incorrect personal information

- Collection accounts you don’t recognize

Take action immediately.

Knowing how to check your credit report for signs of identity theft is important, but responding quickly when you find evidence of fraud is what truly helps protect your credit, finances, and long-term financial health.

For a complete recovery plan, follow our step-by-step guide on What To Do Immediately If Your Identity Is Stolen.

How to Place a Fraud Alert on Your Credit File

If you discover suspicious activity while learning how to check your credit report for signs of identity theft, placing a fraud alert on your credit file is one of the fastest steps you can take to protect yourself.

Not sure whether a fraud alert or security freeze is the better option? Compare both in our Credit Freeze vs Credit Lock guide.

A fraud alert tells lenders that they should take additional steps to verify your identity before approving new credit applications. While a fraud alert does not prevent access to your credit report like a credit freeze does, it can make it more difficult for identity thieves to open accounts using your personal information.

What Is a Fraud Alert?

A fraud alert is a notice placed on your credit file that encourages creditors to verify your identity before issuing new credit.

When a lender sees the alert, they may:

- Contact you directly

- Request additional identification

- Perform extra verification steps

- Delay approval until identity confirmation is completed

Fraud alerts are designed to reduce the risk of unauthorized accounts on a credit report after suspicious financial activity is detected.

When Should You Place a Fraud Alert?

You should consider placing a fraud alert if you notice:

- Fraudulent inquiries

- Unauthorized accounts on a credit report

- Incorrect personal information

- Collection accounts you do not recognize

- Evidence of identity theft

- Personal information exposed in a data breach

Even if fraud has not yet occurred, a fraud alert may provide an extra layer of protection after your information has been compromised.

Types of Fraud Alerts

There are several types of fraud alerts available.

Initial Fraud Alert

An initial fraud alert is often used when:

- You suspect identity theft

- Your information was exposed

- You notice suspicious activity

This alert provides temporary protection while you investigate potential fraud.

Extended Fraud Alert

An extended fraud alert is typically available to confirmed identity theft victims.

This option offers longer-lasting protection and may include additional safeguards against fraudulent credit applications.

How to Place a Fraud Alert

Placing a fraud alert is generally straightforward.

You can contact one of the major credit bureaus:

You will typically need to provide:

- Full name

- Date of birth

- Social Security number

- Current address

- Identity verification information

After verification, the fraud alert can be added to your credit file.

Fraud Alert vs Credit Freeze

Many consumers confuse fraud alerts with credit freezes.

A fraud alert:

- Warns lenders to verify identity

- Allows continued access to your credit file

- Can be placed quickly

A credit freeze:

- Restricts access to your credit reports

- Makes it harder for criminals to open new accounts

- Provides stronger protection against new account fraud

Many identity theft victims choose both options depending on the severity of the situation.

Continue Monitoring Your Credit Reports

Placing a fraud alert should not replace regular monitoring.

Continue reviewing your credit reports for:

- New accounts

- Suspicious activity

- Fraudulent inquiries

- Incorrect addresses

- Unauthorized changes

This ongoing review remains an important part of how to check your credit report for signs of identity theft.

What Happens After a Fraud Alert Is Added?

Once a fraud alert is active, lenders should exercise greater caution when reviewing credit applications.

While this does not guarantee fraud prevention, it can help reduce the likelihood of:

- Fraudulent credit card approvals

- Unauthorized loans

- New account fraud

- Additional identity theft activity

The alert serves as an important warning that your information may be at risk.

Consider Identity Monitoring for Added Protection

Many consumers supplement fraud alerts with identity monitoring services that can provide notifications for:

- New account openings

- Credit report changes

- Hard inquiries

- Personal information updates

- Suspicious financial activity

Early alerts can help you respond quickly if additional fraud occurs.

Fraud Alerts Are Only One Part of Recovery

A fraud alert can be an effective protective measure, but it should be part of a broader identity theft recovery plan that may include:

- Disputing fraudulent information

- Contacting affected lenders

- Monitoring financial accounts

- Freezing credit files

- Using identity protection services

Understanding how fraud alerts work is an important part of how to check your credit report for signs of identity theft. When used alongside regular credit monitoring and prompt fraud response, a fraud alert can help protect your credit and reduce the risk of future identity theft.

How to Freeze Your Credit After Identity Theft

If you discover suspicious activity while learning how to check your credit report for signs of identity theft, freezing your credit may be one of the most effective steps you can take to prevent additional fraud.

A credit freeze restricts access to your credit reports, making it significantly harder for criminals to open new accounts using your personal information. While a credit freeze won’t stop fraud that has already occurred, it can help prevent identity thieves from causing further damage.

What Is a Credit Freeze?

A credit freeze, sometimes called a security freeze, limits who can access your credit report.

When your credit file is frozen:

- Most lenders cannot view your credit report.

- New credit applications are generally blocked.

- Identity thieves have a harder time opening accounts in your name.

- Your existing accounts remain accessible to you.

A credit freeze is widely considered one of the strongest defenses against new account fraud.

When Should You Freeze Your Credit?

You should consider freezing your credit if you find:

- Unauthorized accounts on a credit report

- Fraudulent inquiries

- Incorrect personal information linked to fraud

- Evidence of identity theft

- Exposure from a major data breach

Many experts recommend freezing your credit immediately after discovering confirmed identity theft.

Contact All Three Credit Bureaus

To fully protect your credit, place a freeze with each major credit bureau:

A freeze placed with one bureau does not automatically freeze your files with the others.

Information You’ll Need

When requesting a credit freeze, you may need to provide:

- Full legal name

- Date of birth

- Social Security number

- Current address

- Proof of identity

The verification process helps ensure only you can control access to your credit file.

How a Credit Freeze Protects You

Identity thieves often use stolen information to apply for:

- Credit cards

- Personal loans

- Auto loans

- Retail financing

- Lines of credit

Because lenders typically review credit reports before approving applications, a freeze creates a major obstacle for criminals.

This protection is especially valuable after discovering fraudulent accounts on a credit report.

Can You Still Use Your Credit?

Yes.

A credit freeze does not affect:

- Your credit score

- Existing credit cards

- Existing loans

- Bank accounts

If you need to apply for new credit, you can temporarily lift the freeze with the relevant credit bureau before submitting your application.

Credit Freeze vs Fraud Alert

Many consumers compare credit freezes and fraud alerts after discovering suspicious financial activity.

A fraud alert:

- Warns lenders to verify your identity

- Still allows access to your credit file

- Provides an additional layer of caution

A credit freeze:

- Restricts access to your credit reports

- Blocks many new credit applications

- Offers stronger protection against identity theft

For many victims, a credit freeze provides the highest level of protection.

Continue Monitoring Your Credit Reports

Freezing your credit is important, but it does not eliminate the need for ongoing monitoring.

Continue reviewing your reports for:

- New fraudulent inquiries

- Incorrect personal information

- Collection accounts

- Suspicious activity

- Credit score changes

Regular monitoring remains an essential part of how to check your credit report for signs of identity theft.

Consider Identity Monitoring Services

Many consumers choose identity monitoring services alongside a credit freeze.

These services may help detect:

- New account attempts

- Personal information changes

- Dark web exposure

- Suspicious financial activity

- Identity theft warning signs

Monitoring can provide early alerts that help you respond quickly to future threats.

Keep Records of Your Freeze Requests

After placing a freeze:

- Save confirmation emails.

- Record freeze dates.

- Store any account credentials securely.

- Document future temporary lifts.

Maintaining organized records can make managing your credit freeze easier over time.

Why a Credit Freeze Is Worth Considering

If you’ve already identified suspicious activity, waiting can increase your risk.

Freezing your credit can:

- Reduce future fraud opportunities

- Protect against unauthorized credit applications

- Limit financial damage

- Strengthen your identity theft recovery plan

For many victims, it is one of the most effective actions available after discovering fraud.

Understanding how to check your credit report for signs of identity theft can help you uncover fraud, but freezing your credit can help stop identity thieves from opening additional accounts and causing even more financial damage.

Need detailed instructions? Our complete guide explains exactly How to Freeze Your Credit After Identity Theft from start to finish.

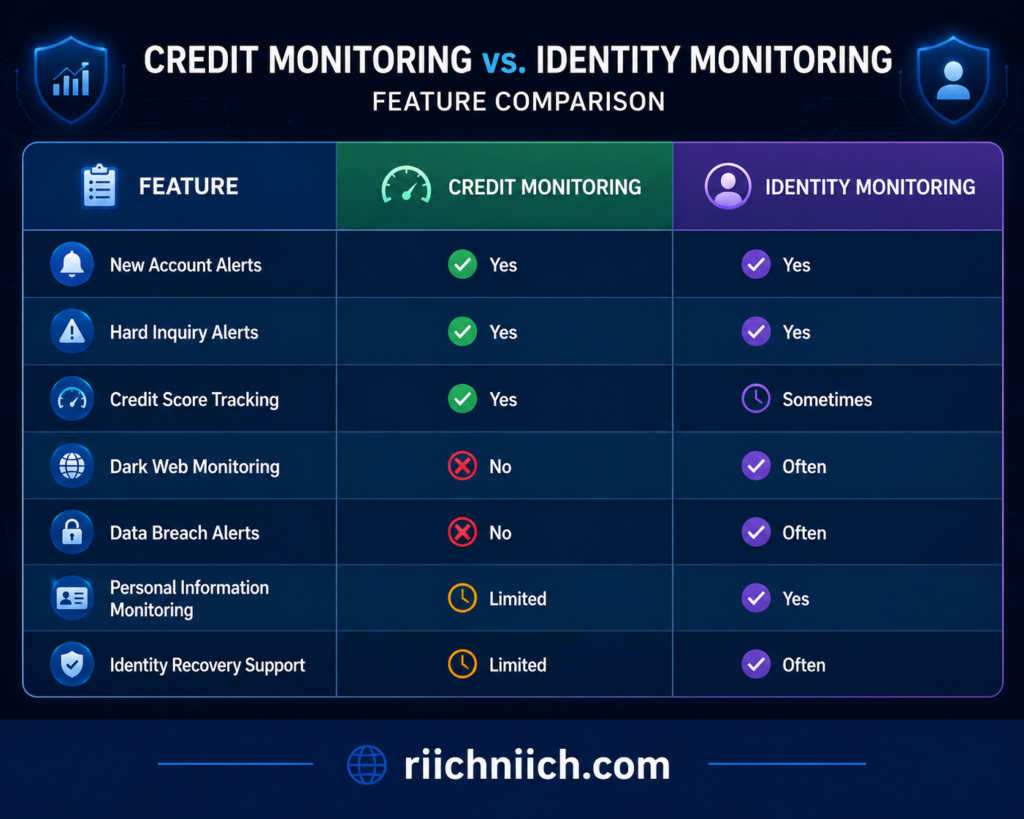

Identity Monitoring vs Credit Monitoring: Which Offers Better Protection?

After learning how to check your credit report for signs of identity theft, many consumers wonder whether they should rely on credit monitoring, identity monitoring, or both. While these services are often mentioned together, they are not the same.

Understanding the difference can help you choose the right level of protection for your personal information and financial accounts.

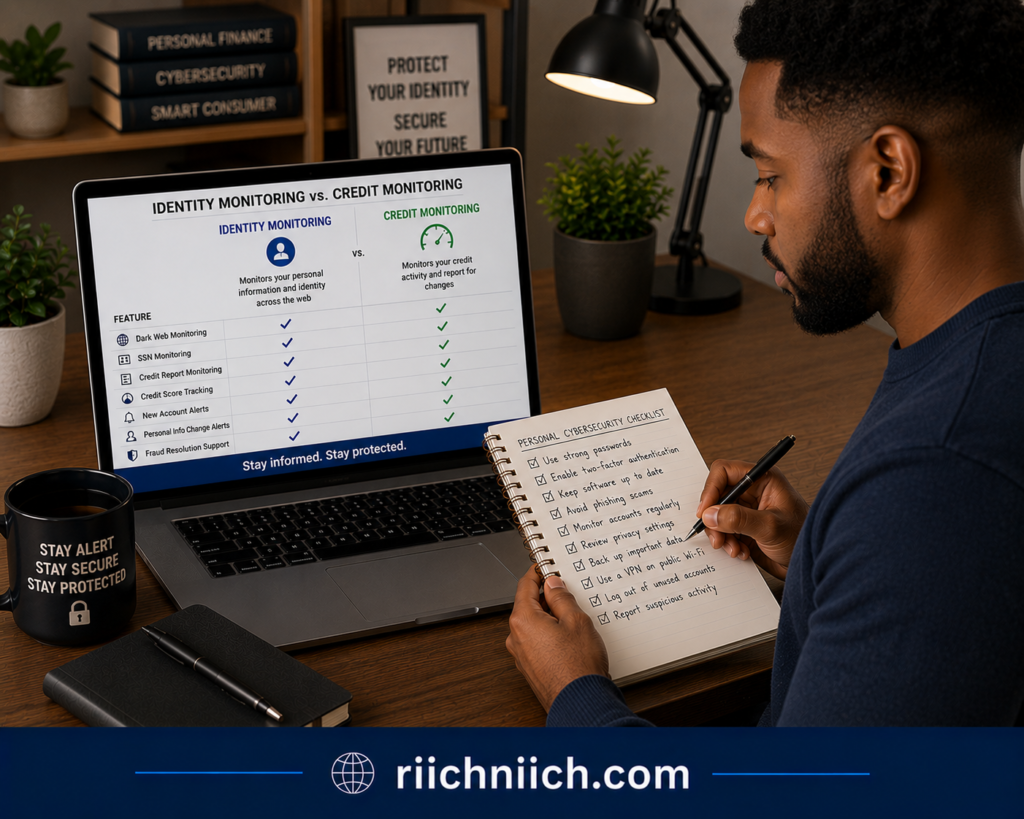

What Is Credit Monitoring?

Credit monitoring focuses primarily on changes that occur within your credit files.

Typical credit monitoring alerts may include:

- New credit accounts

- Hard inquiries

- Credit score changes

- New collection accounts

- Significant credit report updates

Credit monitoring can help you identify fraudulent accounts on a credit report and detect suspicious financial activity after it appears on your credit file.

What Is Identity Monitoring?

Identity monitoring provides broader protection by monitoring various sources for signs that your personal information is being misused.

Depending on the service, identity monitoring may track:

- Social Security number usage

- Dark web exposure

- Personal information changes

- Data breach notifications

- Criminal record monitoring

- Financial account monitoring

- Identity theft warning signs

Identity monitoring aims to detect threats before they evolve into credit-related fraud.

Key Difference Between the Two

The biggest difference is timing.

Credit monitoring often alerts you after suspicious activity affects your credit report.

Identity monitoring may help identify risks before fraudulent accounts on a credit report are opened.

For consumers concerned about identity theft, earlier detection can be extremely valuable.

Credit Monitoring Pros

Benefits of credit monitoring include:

- Tracks credit file activity

- Alerts for new accounts

- Monitors hard inquiries

- Helps detect credit report fraud

- Usually easy to set up

Credit monitoring can be particularly useful after you’ve learned how to check your credit report for signs of identity theft and want ongoing visibility into your credit files.

Credit Monitoring Limitations

Credit monitoring does have limitations.

It generally does not monitor:

- Dark web activity

- Data breaches

- Personal information exposure

- Non-credit identity theft

This means identity theft may occur before a credit monitoring service generates an alert.

Identity Monitoring Pros

Identity monitoring provides broader coverage.

Potential benefits include:

- Monitoring exposed personal information

- Tracking dark web activity

- Data breach notifications

- Earlier fraud detection

- Identity recovery assistance

These features can help consumers identify suspicious activity before significant financial damage occurs.

Identity Monitoring Limitations

Identity monitoring is powerful, but it cannot prevent all forms of fraud.

Consumers should still:

- Review credit reports regularly

- Monitor financial accounts

- Use strong passwords

- Freeze credit when necessary

Identity monitoring works best as part of a larger identity protection strategy.

Which Offers Better Protection?

For most consumers, identity monitoring provides broader protection because it covers more than just credit activity.

Credit monitoring helps answer questions like:

- Were new accounts opened?

- Did someone submit a credit application?

- Has my credit score changed?

Identity monitoring expands protection by helping answer:

- Was my personal information exposed?

- Did my data appear on the dark web?

- Has someone attempted to misuse my identity?

Because identity theft often begins before credit activity occurs, identity monitoring may provide earlier warnings.

Why Many Consumers Use Both

The strongest protection often comes from combining:

- Regular credit report reviews

- Credit monitoring

- Identity monitoring

- Fraud alerts

- Credit freezes

Together, these tools create multiple layers of defense against identity theft.

How These Services Support Credit Report Reviews

Even with monitoring services, you should still practice how to check your credit report for signs of identity theft regularly.

Monitoring services are designed to complement—not replace—manual reviews.

Consumers should continue looking for:

- Unauthorized accounts on a credit report

- Fraudulent inquiries

- Incorrect addresses

- Collection accounts

- Suspicious financial activity

Who Should Consider Identity Monitoring?

Identity monitoring may be especially valuable if:

- You’ve experienced identity theft before.

- Your information was exposed in a data breach.

- You frequently shop online.

- You want proactive fraud alerts.

- You maintain multiple financial accounts.

For many consumers, the added visibility can provide peace of mind and faster fraud detection.

Final Comparison

Understanding the difference between these services can strengthen your overall protection strategy. While both tools have value, combining identity monitoring with the practices taught in how to check your credit report for signs of identity theft can help you identify threats earlier and reduce the risk of long-term financial damage.

We also compare these services in greater detail in our Identity Monitoring vs Credit Monitoring guide to help you choose the right protection.

How Identity Theft Protection Services Can Help Detect Fraud Faster

Learning how to check your credit report for signs of identity theft is one of the best ways to uncover fraud, but many consumers only review their reports occasionally. Unfortunately, identity thieves can open accounts, submit credit applications, or misuse personal information long before a manual review takes place.

This is where identity theft protection services can provide additional value. These services continuously monitor various sources for suspicious activity and can alert you when potential fraud is detected, helping you respond faster and limit financial damage.

Why Early Detection Matters

The longer identity theft goes unnoticed, the greater the potential damage.

Criminals may:

- Open multiple credit accounts

- Submit fraudulent loan applications

- Change personal information

- Accumulate debt

- Damage your credit score

Early detection can make the recovery process significantly easier and reduce the overall impact of identity theft.

How Identity Theft Protection Services Work

Identity theft protection services monitor your personal information for signs of misuse.

Depending on the provider, monitoring may include:

- Credit report activity

- New account openings

- Hard inquiries

- Dark web monitoring

- Social Security number monitoring

- Personal information changes

- Data breach notifications

When suspicious activity is detected, you may receive an alert so you can investigate quickly.

Faster Detection Than Manual Reviews

Even if you understand how to check your credit report for signs of identity theft, most people do not check their reports every day.

Identity theft protection services help bridge this gap by providing ongoing monitoring between credit report reviews.

Instead of waiting weeks or months to discover fraud, you may receive notifications shortly after suspicious activity occurs.

Alerts for New Credit Activity

One of the most valuable features of many services is new account monitoring.

Alerts may be triggered by:

- Credit card applications

- Personal loan applications

- Auto financing requests

- New lines of credit

- Hard inquiries

These alerts can help identify fraudulent accounts on a credit report before they cause significant harm.

Monitoring Personal Information Changes

Identity thieves often modify personal information before opening accounts.

Monitoring services may alert you to:

- Address changes

- Name changes

- Contact information updates

- Social Security number activity

These early warning signs may appear before unauthorized accounts on a credit report are created.

Dark Web Monitoring

Many identity theft protection services include dark web monitoring.

This feature searches for exposed personal information such as:

- Email addresses

- Passwords

- Social Security numbers

- Financial account information

If your information appears in a data breach or criminal marketplace, you may receive an alert that allows you to take preventive action.

Identity Theft Recovery Assistance

Detection is important, but recovery support can be equally valuable.

Many services provide access to specialists who can assist with:

- Fraud reports

- Credit bureau disputes

- Account recovery

- Identity restoration

- Recovery planning

This support can help simplify the recovery process after identity theft occurs.

Are Identity Theft Protection Services a Replacement for Credit Report Reviews?

No.

Identity theft protection services should complement—not replace—your efforts to learn how to check your credit report for signs of identity theft.

You should still review your credit reports regularly for:

- Fraudulent inquiries

- Unauthorized accounts on a credit report

- Collection accounts

- Incorrect personal information

- Suspicious financial activity

Combining monitoring services with manual reviews provides stronger protection than either approach alone.

Who Benefits Most From Identity Theft Protection?

Identity theft protection services may be especially useful for:

- Data breach victims

- Frequent online shoppers

- Families managing multiple accounts

- Seniors

- Individuals with extensive financial activity

- Consumers who want ongoing monitoring

For many people, the ability to receive early alerts provides valuable peace of mind.

Features to Look For

When comparing identity theft protection services, consider features such as:

- Credit monitoring

- Identity monitoring

- Dark web monitoring

- Fraud alerts

- Recovery assistance

- Financial account monitoring

- Identity theft insurance

If you’re comparing providers, see our roundup of the Best Identity Theft Protection Services to find the right option for your needs.

A Layered Approach Provides the Best Protection

No single tool can completely prevent identity theft.

The strongest protection strategy often includes:

- Regular credit report reviews

- Fraud alerts

- Credit freezes

- Strong passwords

- Multi-factor authentication

- Identity theft protection services

Together, these measures can reduce your risk and improve your ability to detect fraud quickly.

Understanding how to check your credit report for signs of identity theft remains essential, but identity theft protection services can provide an additional layer of defense by monitoring for suspicious activity, delivering early alerts, and helping you respond before identity theft causes serious financial damage.

Common Mistakes to Avoid When Checking Your Credit Report

Understanding how to check your credit report for signs of identity theft is an important skill, but many consumers unknowingly overlook critical details that could reveal fraud. Even small mistakes can allow identity theft to go undetected for months, giving criminals more time to open accounts, accumulate debt, and damage your credit.

By avoiding the common mistakes below, you can improve your ability to detect suspicious activity and identify fraudulent accounts on a credit report before they become major financial problems.

Mistake #1: Only Looking at Your Credit Score

Many people check their credit score and assume everything is fine if the number looks normal.

However, your credit score alone cannot reveal:

- Unauthorized accounts on a credit report

- Incorrect personal information

- Fraudulent inquiries

- Collection accounts

The real value comes from reviewing the entire credit report, not just the score.

Mistake #2: Reviewing Only One Credit Bureau Report

Some consumers check a single credit report and ignore the others.

Because lenders report information differently, fraudulent activity may appear on:

- Experian

- Equifax

- TransUnion

at different times.

A critical part of how to check your credit report for signs of identity theft is reviewing reports from all three major credit bureaus.

Mistake #3: Ignoring Small or Unfamiliar Accounts

Identity thieves often begin with smaller accounts because they are less likely to attract attention.

Don’t ignore:

- Store credit cards

- Small loans

- Retail financing accounts

- Low-limit credit lines

Even minor accounts can be important identity theft warning signs.

Mistake #4: Overlooking Personal Information Changes

Many consumers focus exclusively on financial accounts.

However, suspicious changes to:

- Addresses

- Employers

- Phone numbers

- Name variations

can be early indicators of identity theft.

Review every section of your report carefully.

Mistake #5: Dismissing Unknown Credit Inquiries

Fraudulent inquiries are often among the first signs that criminals are attempting to use your identity.

Some consumers assume inquiries are harmless and ignore them.

Always investigate:

- Hard inquiries

- Unfamiliar lenders

- Multiple recent inquiries

- Applications you did not authorize

These entries may indicate attempted account fraud.

Mistake #6: Waiting Too Long Between Reviews

Checking your credit report once every few years is not enough.

Identity theft can develop quickly.

Regular reviews help you identify:

- Fraudulent accounts on a credit report

- Suspicious financial activity

- Credit report fraud

- Unauthorized inquiries

The sooner fraud is discovered, the easier it is to stop.

Mistake #7: Failing to Save Previous Reports

Many consumers review their reports and then discard them.

Keeping copies allows you to:

- Compare account activity

- Spot new inquiries

- Identify address changes

- Track suspicious activity over time

Historical comparisons often reveal changes that might otherwise be missed.

Mistake #8: Assuming Errors Are Harmless

Not every error indicates identity theft, but every unexplained error deserves attention.

Examples include:

- Incorrect addresses

- Unknown employers

- Misspelled names

- Unfamiliar accounts

Ignoring inaccuracies may allow fraudulent activity to continue undetected.

Mistake #9: Not Taking Action After Discovering Problems

Finding suspicious information is only the first step.

Some consumers delay action because they assume the issue will resolve itself.

If you discover fraud:

- Contact affected lenders

- Dispute inaccurate information

- Consider a fraud alert

- Consider a credit freeze

- Monitor your accounts closely

Fast action can significantly reduce financial damage.

Mistake #10: Relying Solely on Monitoring Services

Identity monitoring and credit monitoring can be valuable tools, but they should not replace manual reviews.

Monitoring services may help detect:

- New account openings

- Personal information changes

- Suspicious activity

However, consumers should still practice how to check your credit report for signs of identity theft regularly to verify information and identify potential problems themselves.

Build a Strong Review Routine

The most effective approach combines:

- Credit report reviews

- Credit monitoring

- Identity monitoring

- Fraud alerts

- Credit freezes when necessary

A layered approach improves your chances of detecting fraud early and protecting your financial future.

Quick Credit Report Review Checklist

Before finishing your review, confirm that you checked:

✅ Personal information

✅ Addresses

✅ Employers

✅ Credit accounts

✅ Hard inquiries

✅ Collection accounts

✅ Credit score changes

✅ New activity since your last review

Avoiding these mistakes can significantly improve your ability to detect fraud. By understanding how to check your credit report for signs of identity theft and reviewing your reports thoroughly, you can uncover suspicious activity earlier and take action before identity theft causes serious financial consequences.

Frequently Asked Questions About Checking Your Credit Report for Identity Theft

Reviewing your credit reports is one of the most effective ways to detect identity theft early. Below are answers to some of the most common questions people have about how to check your credit report for signs of identity theft and protect themselves from fraudulent activity.

How often should I check my credit report for identity theft?

At a minimum, you should review your credit reports several times throughout the year.

You may want to check more frequently if:

- You were affected by a data breach

- You received a fraud alert

- You suspect identity theft

- Your personal information was exposed online

- You notice suspicious financial activity

Regular reviews improve your chances of identifying fraudulent accounts on a credit report before serious damage occurs.

What is the biggest warning sign of identity theft on a credit report?

The most obvious warning sign is finding an account you did not open.

Other common identity theft warning signs include:

- Fraudulent inquiries

- Collection accounts you don’t recognize

- Incorrect addresses

- Unknown employers

- Unexpected credit score drops

Any unfamiliar information should be investigated immediately.

Can someone steal my identity without opening a credit account?

Yes.

Identity theft does not always involve new credit accounts.

Criminals may use your information to:

- File fraudulent tax returns

- Access financial accounts

- Commit medical fraud

- Obtain employment

- Conduct other forms of identity fraud

This is why identity monitoring services can provide protection beyond traditional credit monitoring.

Do credit reports show all types of identity theft?

No.

Credit reports are excellent for detecting:

- Unauthorized accounts on a credit report

- Fraudulent inquiries

- Collection accounts

- Suspicious financial activity

However, they may not reveal:

- Tax fraud

- Criminal identity theft

- Medical identity theft

- Certain account takeover attacks

A comprehensive identity protection strategy often includes additional monitoring tools.

Will checking my own credit report hurt my credit score?

No.

When you request your own credit report, it creates a soft inquiry.

Soft inquiries do not impact your credit score.

Reviewing your reports regularly is an important part of how to check your credit report for signs of identity theft and carries no credit score penalty.

What should I do if I find an account I don’t recognize?

Take action immediately.

Recommended steps include:

- Contact the lender.

- Document the account details.

- File disputes with the credit bureaus.

- Place a fraud alert if appropriate.

- Consider freezing your credit files.

- Report identity theft through IdentityTheft.gov.

Quick action can help limit financial losses and prevent additional fraud.

What if I find a fraudulent inquiry but no account?

Fraudulent inquiries often occur before new accounts are approved.

An unfamiliar inquiry may indicate:

- Attempted identity theft

- A denied application

- Misuse of your personal information

Even if no account exists yet, you should investigate and monitor your reports closely.

What’s the difference between credit monitoring and identity monitoring?

Credit monitoring focuses primarily on:

- Credit report changes

- New accounts

- Hard inquiries

- Credit score activity

Identity monitoring may also track:

- Personal information exposure

- Dark web activity

- Data breach notifications

- Social Security number monitoring

Many consumers use both services for broader protection.

Should I freeze my credit if I discover identity theft?

Many experts recommend freezing your credit after confirmed identity theft.

A credit freeze can:

- Restrict access to your credit reports

- Make it harder for criminals to open accounts

- Reduce future fraud opportunities

The decision depends on your specific situation, but it is often one of the strongest identity theft recovery tools available.

Can identity theft protection services replace checking my credit report?

No.

Identity theft protection services can provide valuable alerts, but they should not replace manual credit report reviews.

You should continue practicing how to check your credit report for signs of identity theft by reviewing your reports regularly and looking for:

- Unauthorized accounts on a credit report

- Fraudulent inquiries

- Incorrect personal information

- Collection accounts

- Suspicious activity

Combining monitoring services with regular reviews offers stronger protection.

How long can fraudulent information remain on my credit report?

If left unreported, fraudulent information may remain on your credit report for an extended period.

The sooner you identify and dispute inaccurate information, the faster you can begin correcting your credit file and limiting potential damage.

Where can I get my credit reports?

Consumers can obtain their reports through:

You can also learn more about identity theft recovery through:

Understanding these common questions can help you better protect your personal information. By consistently applying how to check your credit report for signs of identity theft, you can detect fraud earlier, respond faster, and reduce the risk of long-term financial damage.

Conclusion: How to Check Your Credit Report for Signs of Identity Theft

Identity theft can happen to anyone, and in many cases, victims don’t discover the problem until significant financial damage has already occurred. That’s why learning how to check your credit report for signs of identity theft is one of the most important habits you can develop for protecting your financial future.

By reviewing your credit reports regularly, you can identify:

- Unauthorized accounts on a credit report

- Fraudulent inquiries

- Incorrect personal information

- Collection accounts you don’t recognize

- Suspicious financial activity

- Identity theft warning signs

The earlier these issues are discovered, the easier they are to resolve.

The Most Effective Protection Strategy

No single tool can completely prevent identity theft.

The strongest approach combines:

- Regular credit report reviews

- Credit monitoring

- Identity monitoring

- Fraud alerts

- Credit freezes when necessary

- Strong password practices

- Multi-factor authentication

Together, these layers help reduce the risk of fraud while improving your ability to detect problems quickly.

Why Credit Report Reviews Still Matter

Even with monitoring services and fraud alerts, manually reviewing your credit reports remains essential.

Monitoring tools can provide valuable alerts, but only you can fully verify:

- Whether an account belongs to you

- Whether an inquiry was authorized

- Whether personal information is accurate

- Whether suspicious activity requires action