How to freeze your credit after identity theft is one of the most important steps you can take to protect yourself from further fraud. If criminals have gained access to your personal information, freezing your credit can help prevent them from opening new credit cards, loans, or other financial accounts in your name. If you’re not sure whether your information has already been misused, read our guide on How to Know If Someone Stole Your Identity.

In this guide, you’ll learn exactly how a credit freeze works, how to place a freeze with all three major credit bureaus, the difference between a credit freeze and a fraud alert, and additional steps you can take to strengthen your identity theft recovery plan. By the end, you’ll have a clear roadmap for protecting your credit and reducing the risk of future identity theft.

Table of Contents

What Does It Mean to Freeze Your Credit After Identity Theft?

When learning how to freeze your credit after identity theft, it’s important to understand what a credit freeze actually does and why it is one of the most effective ways to stop further fraud.

A credit freeze, also known as a security freeze, restricts access to your credit report at the three major credit bureaus—Equifax, Experian, and TransUnion. When lenders cannot access your credit file, they usually cannot approve new credit cards, loans, or other accounts in your name.

This is especially important after identity theft because criminals often try to use stolen personal information to open new accounts before the victim realizes what has happened.

If someone has already stolen your Social Security number, date of birth, or other personal details, learning how to freeze your credit after identity theft can help prevent additional financial damage. A credit freeze does not remove fraudulent accounts that already exist, but it can stop identity thieves from opening new accounts using your information.

Many people confuse a credit freeze with a fraud alert. While both offer protection, a credit freeze provides a stronger level of security because creditors generally cannot access your credit file until you temporarily lift the freeze.

Key benefits of a credit freeze include:

- Preventing unauthorized credit applications

- Reducing the risk of new account fraud

- Protecting your credit profile after a data breach

- Adding an extra layer of security to identity theft recovery

- Maintaining protection without affecting your credit score

One of the biggest misconceptions is that a credit freeze will lower your credit score. Fortunately, this is not true. Freezing your credit report does not impact your credit score, credit history, or existing accounts.

While a credit freeze is a powerful tool, it should be part of a broader identity theft recovery strategy. Many victims choose to combine a credit freeze with identity monitoring services that can alert them to suspicious activity, dark web exposure, and unauthorized use of their personal information.

Understanding how to freeze your credit after identity theft is often one of the first and most important steps in protecting yourself from additional fraud. In the next section, we’ll look at why acting quickly can make a significant difference after your identity has been compromised.

Why You Should Freeze Your Credit Immediately After Identity Theft

If you’ve become a victim of identity theft, time matters. The sooner you learn how to freeze your credit after identity theft, the better your chances of preventing additional fraud and financial damage.

Identity thieves often move quickly. Once they gain access to sensitive information such as your Social Security number, date of birth, or financial account details, they may attempt to open new credit cards, personal loans, auto loans, or other accounts in your name. In many cases, victims don’t discover the fraud until weeks or even months later.

A credit freeze helps stop this process by restricting access to your credit report. Because most lenders review your credit file before approving new accounts, freezing your credit report makes it significantly harder for criminals to use your stolen information.

One of the biggest reasons to understand how to freeze your credit after identity theft is that it creates an immediate barrier between your personal information and potential lenders. Even if a criminal has enough information to submit a credit application, the lender will likely be unable to access the credit report needed to approve it.

A credit freeze helps block new credit applications, but it won’t alert you if criminals continue using your personal information elsewhere.

👉 That’s why many identity theft victims use Aura to monitor their credit, identity, and dark web exposure in real time.

Identity Thieves Often Strike More Than Once

Many victims assume that identity theft is a one-time event. Unfortunately, that’s rarely the case. Understanding How Identity Theft Happens can help you reduce the risk of becoming a repeat victim.

Once personal information has been exposed through a data breach, phishing scam, stolen mail, or hacked account, criminals may continue attempting to exploit that information for months or years. This is why placing a credit freeze should be considered one of the first identity theft recovery steps.

A credit freeze can help protect against:

- New credit card fraud

- Personal loan fraud

- Auto loan fraud

- Unauthorized financing applications

- Synthetic identity fraud

- Multiple fraudulent account openings

A Credit Freeze Costs Nothing

Another reason to act immediately is that federal law allows consumers to place a credit freeze for free with Equifax, Experian, and TransUnion.

There is no fee to freeze your credit report, temporarily lift the freeze, or permanently remove it later if needed. Since the process is free and can provide substantial protection, delaying action often creates unnecessary risk.

A Credit Freeze Does Not Affect Your Credit Score

Many people hesitate because they worry about harming their credit score. Fortunately, freezing your credit has no impact on your credit score, existing credit cards, bank accounts, or loan payments.

You can continue using your current accounts normally while keeping your credit file protected from new account fraud.

Consider Additional Monitoring Protection

While learning how to freeze your credit after identity theft is essential, a credit freeze alone cannot alert you to every type of fraud. For example, it won’t notify you if your personal information appears on the dark web or if suspicious activity occurs on existing accounts.

This is why many identity theft victims also use identity monitoring services that provide:

- Credit monitoring alerts

- Dark web monitoring

- Identity theft notifications

- Fraud activity detection

- Identity restoration assistance

Combining a credit freeze with ongoing monitoring creates a stronger defense against future identity theft attempts.

Taking immediate action can make a significant difference after identity theft. Understanding how to freeze your credit after identity theft and acting quickly may prevent criminals from causing even greater financial harm while you work to recover and secure your personal information.

Step 1: Gather the Information You Need

Before you begin how to freeze your credit after identity theft, it’s important to gather the necessary information. Having everything ready beforehand will make the process faster and help you avoid delays when verifying your identity with the credit bureaus.

The three major credit bureaus—Equifax, Experian, and TransUnion—must confirm that you are the rightful owner of the credit file before allowing you to place a credit freeze. This security step helps prevent unauthorized individuals from making changes to your credit report.

Information You Will Typically Need

Most credit bureaus will ask for the following:

- Full legal name

- Date of birth

- Social Security number

- Current home address

- Previous addresses (if applicable)

- Email address

- Phone number

Make sure the information matches what appears on your credit reports. Even small discrepancies can slow down the verification process.

Gather Supporting Documents

In some situations, especially if you’ve recently moved or your information has changed, the credit bureau may request additional documentation to verify your identity.

Examples include:

- Driver’s license or state-issued ID

- Passport

- Utility bill

- Bank statement

- Insurance statement

- Government-issued correspondence

Having digital copies available can make it easier to complete online verification requests.

Review Your Credit Reports First

As part of how to freeze your credit after identity theft, it’s also a good idea to review your credit reports before placing the freeze.

Look for:

- Accounts you don’t recognize

- Unauthorized credit inquiries

- Incorrect personal information

- New credit cards or loans you didn’t open

- Collection accounts that don’t belong to you

You should also review these 13 Warning Signs Someone Stole Your Identity to identify fraud that may have gone unnoticed.

Identifying suspicious activity early can help you take additional recovery steps if needed.

You can access your free credit reports through the Annual Credit Report website, which is authorized by federal law.

Create a Secure Record of Your Information

Once you successfully place a credit freeze, you’ll receive account details and confirmation information from each credit bureau. You’ll need these credentials later if you want to temporarily lift your credit freeze when applying for a mortgage, car loan, apartment, or credit card.

Many consumers store this information in a secure password manager to keep it protected and easily accessible.

Don’t Wait if Identity Theft Has Already Occurred

If you’ve already noticed fraudulent activity, don’t spend days gathering paperwork before taking action. Collect the essential information you need and begin the process as soon as possible.

The faster you complete how to freeze your credit after identity theft, the sooner you can reduce the risk of criminals opening additional accounts in your name.

Once you have your information ready, you’re prepared to place a credit freeze with each of the three major credit bureaus, starting with Equifax.

Step 2: Place a Credit Freeze With Equifax

A critical part of how to freeze your credit after identity theft is placing a credit freeze with Equifax. Since lenders may use different credit bureaus when reviewing applications, freezing your Equifax credit report helps prevent identity thieves from opening new accounts using information tied to your Equifax file.

The fastest way to place a credit freeze is through Equifax’s online security freeze system. You can also request a freeze by phone or mail, but online requests are usually processed much faster.

How to Place a Credit Freeze With Equifax

To freeze your credit report with Equifax:

- Visit the official Equifax credit freeze page.

- Create an Equifax account or sign in to an existing account.

- Verify your identity using the requested personal information.

- Submit your security freeze request.

- Save your confirmation details and login credentials.

After your identity is verified, the credit freeze is typically activated quickly, helping restrict access to your credit file.

What Happens After the Freeze Is Active?

Once the Equifax credit freeze is in place, most lenders will be unable to access your Equifax credit report when reviewing new credit applications. As a result, identity thieves may have a much harder time opening:

- Credit cards

- Personal loans

- Auto loans

- Store financing accounts

- Other forms of credit

This added protection is one of the main reasons experts recommend how to freeze your credit after identity theft as one of the first recovery steps.

Keep Your Equifax Account Information Safe

After placing your freeze, Equifax will provide account access information that you’ll need if you decide to:

- Temporarily lift your credit freeze

- Permanently remove your credit freeze

- Apply for new credit in the future

Store this information securely so you can easily access it when needed.

Remember: Equifax Is Only One Part of the Process

Many people mistakenly believe that freezing their credit with a single bureau provides complete protection. Unfortunately, that’s not the case.

To fully complete how to freeze your credit after identity theft, you’ll also need to place a credit freeze with Experian and TransUnion. Each bureau maintains its own credit file, and lenders may use any one of them when evaluating credit applications.

For official instructions and current freeze options, visit the Equifax Security Freeze Center.

Once your Equifax credit freeze is active, you’re ready to move on to the next step: placing a credit freeze with Experian.

Step 3: Place a Credit Freeze With Experian

The next step in how to freeze your credit after identity theft is placing a credit freeze with Experian. Just like Equifax, Experian maintains its own credit file, and many lenders use Experian credit reports when evaluating credit applications.

If you skip this step, identity thieves may still be able to apply for credit through lenders that rely primarily on Experian data. That’s why a complete credit freeze strategy always includes all three major credit bureaus.

How to Place a Credit Freeze With Experian

Experian allows consumers to freeze their credit report online, by phone, or by mail. The online option is usually the fastest and most convenient.

To place your credit freeze:

- Visit the official Experian credit freeze page.

- Create an account or sign in to your existing Experian account.

- Complete the identity verification process.

- Submit your security freeze request.

- Save all account details and confirmation information.

Once approved, the freeze helps restrict access to your Experian credit report and can help prevent unauthorized credit applications.

Why Freezing Your Experian Credit Report Matters

When people research how to freeze your credit after identity theft, they often assume that freezing one bureau is enough. Unfortunately, lenders don’t all use the same credit bureau.

Some creditors may pull reports from:

- Experian

- Equifax

- TransUnion

- Multiple bureaus simultaneously

By freezing your Experian credit report, you close another potential entry point that identity thieves could use to open fraudulent accounts.

Keep Track of Your Freeze Status

After placing the freeze, verify that your Experian account reflects an active security freeze.

You should also maintain records of:

- Freeze confirmation emails

- Account usernames

- Passwords

- Security questions

- Recovery information

Keeping these details organized will make it easier if you need to temporarily lift your freeze for a future loan, mortgage application, apartment rental, or credit card approval.

Continue Monitoring for Fraud

Even after freezing your Experian credit report, you should continue watching for signs of identity theft.

A credit freeze helps stop new account fraud, but it does not automatically detect:

- Existing account takeover attempts

- Dark web exposure

- Suspicious banking activity

- Fraud involving current accounts

This is why many victims who complete how to freeze your credit after identity theft also use credit monitoring and identity monitoring services to receive alerts about potential threats.

For current instructions and security freeze options, visit the Experian Security Freeze Center.

Once your Experian credit freeze is active, you are one step closer to fully protecting your credit profile. The final bureau you need to secure is TransUnion, which we’ll cover next.

Step 4: Place a Credit Freeze With TransUnion

The final step in how to freeze your credit after identity theft is placing a credit freeze with TransUnion. Once you’ve completed freezes with Equifax, Experian, and TransUnion, you’ll have the strongest level of credit-file protection available against new account fraud.

Many identity theft victims mistakenly stop after freezing one or two credit reports. However, because lenders can choose which credit bureau to use when reviewing applications, leaving your TransUnion credit report unfrozen may still create an opportunity for criminals to open accounts using your stolen information.

How to Place a Credit Freeze With TransUnion

TransUnion allows consumers to place a security freeze online, by phone, or by mail. Most people find the online process to be the quickest and easiest option.

To freeze your credit report with TransUnion:

- Visit the official TransUnion credit freeze page.

- Create a TransUnion account or sign in.

- Verify your identity using the requested information.

- Submit your credit freeze request.

- Save your account information and freeze confirmation details.

Once activated, the credit freeze helps restrict access to your TransUnion credit report, making it more difficult for identity thieves to obtain new credit in your name.

Verify That All Three Credit Freezes Are Active

Successfully completing how to freeze your credit after identity theft means confirming that all three major credit bureaus have active freezes in place.

Your protection checklist should look like this:

- Equifax credit freeze active

- Experian credit freeze active

- TransUnion credit freeze active

When all three freezes are active, most lenders will be unable to access your credit reports for new applications unless you temporarily lift the freeze.

Save Your TransUnion Credentials

Just like the other credit bureaus, TransUnion will provide account access information that you’ll need in the future.

Keep a secure record of:

- Usernames

- Passwords

- Security questions

- Freeze confirmation numbers

- Recovery information

You may need these details later when applying for:

- A mortgage

- An auto loan

- A credit card

- Apartment rentals

- Other financing opportunities

Your Credit Freeze Is Now Complete

Once you’ve finished all three bureaus, you’ve successfully completed one of the most important steps in how to freeze your credit after identity theft.

However, it’s important to remember that a credit freeze primarily protects against new account fraud. It does not:

- Monitor your existing financial accounts

- Alert you to dark web exposure

- Detect account takeover attempts

- Notify you about future data breaches

Because of these limitations, many identity theft victims choose to combine a credit freeze with identity monitoring services that provide ongoing alerts and fraud detection.

Continue Monitoring Your Identity

After completing your credit freeze, continue checking your credit reports and financial accounts regularly. Ongoing vigilance can help you identify suspicious activity before it becomes a larger problem.

For official guidance and current freeze instructions, visit the TransUnion Credit Freeze Center.

With your Equifax, Experian, and TransUnion credit freezes now active, you’ve taken a major step toward protecting your financial future and reducing the risk of additional identity theft-related damage.

What Happens After You Freeze Your Credit?

After completing how to freeze your credit after identity theft, many people wonder what changes and what they should expect moving forward. The good news is that a credit freeze begins protecting your credit file almost immediately, making it much harder for identity thieves to open new accounts using your personal information.

However, a credit freeze doesn’t lock down every aspect of your financial life. Understanding exactly what happens next can help you avoid surprises and continue protecting yourself from fraud.

Most New Credit Applications Will Be Blocked

The biggest change is that lenders generally won’t be able to access your credit report while the freeze is active.

Since most financial institutions review your credit file before approving applications, a freeze can help prevent criminals from opening:

- Credit cards

- Personal loans

- Auto loans

- Store financing accounts

- Lines of credit

This is one of the primary reasons experts recommend how to freeze your credit after identity theft as an immediate response to identity theft and data breaches.

Your Existing Accounts Continue Working Normally

One common misconception is that freezing your credit affects your current accounts. Fortunately, that’s not how a credit freeze works.

You can continue using:

- Existing credit cards

- Bank accounts

- Mortgages

- Auto loans

- Investment accounts

Your monthly payments, account balances, and account access remain unchanged.

Your Credit Score Will Not Be Affected

Another concern people have after learning how to freeze your credit after identity theft is whether a credit freeze hurts their credit score.

The answer is no.

A credit freeze does not:

- Lower your credit score

- Change your credit history

- Affect your payment history

- Impact your credit utilization

Your credit score will continue to rise or fall based on your normal financial behavior.

You Can Temporarily Lift the Freeze When Needed

If you apply for a new credit card, mortgage, apartment lease, or loan in the future, you’ll likely need to temporarily lift your credit freeze.

Most credit bureaus allow you to:

- Lift the freeze for a specific lender

- Temporarily unfreeze your credit report

- Remove the freeze permanently if desired

This flexibility allows you to maintain protection while still accessing credit when necessary.

You Should Continue Monitoring Your Credit

Although how to freeze your credit after identity theft provides strong protection against new account fraud, it doesn’t monitor your identity or alert you to suspicious activity.

A credit freeze does not notify you if:

- Your personal information appears on the dark web

- Existing accounts are compromised

- Fraudulent charges occur

- Criminals attempt account takeovers

- New data breaches expose your information

Because of these limitations, many consumers use identity monitoring and credit monitoring services alongside a credit freeze.

Identity Theft Recovery Doesn’t End With a Credit Freeze

A credit freeze is one of the strongest defenses available, but it should be viewed as one part of a larger identity theft recovery plan.

Additional steps may include:

- Monitoring credit reports regularly

- Reviewing financial statements

- Updating passwords

- Enabling multi-factor authentication

- Watching for suspicious emails and phishing attempts

- Using identity theft protection services

Successfully completing how to freeze your credit after identity theft is a major step toward protecting yourself, but ongoing vigilance and monitoring can provide an additional layer of security against future identity theft attempts.

Does a Credit Freeze Hurt Your Credit Score?

One of the most common questions people ask when researching how to freeze your credit after identity theft is whether a credit freeze will damage their credit score. Fortunately, the answer is simple: No, a credit freeze does not hurt your credit score.

Many consumers hesitate to place a credit freeze because they worry it will negatively impact their ability to borrow money in the future. In reality, a credit freeze is a security measure that restricts access to your credit report—it does not change the information contained within it.

How a Credit Freeze Affects Your Credit Report

A credit freeze prevents most lenders from viewing your credit file when evaluating new applications. However, the freeze does not alter important factors that influence your credit score, such as:

- Payment history

- Credit utilization

- Length of credit history

- Credit mix

- Existing account balances

- Credit age

Because these factors remain unchanged, your credit score continues to function normally even after completing how to freeze your credit after identity theft.

What a Credit Freeze Does Not Do

A credit freeze will not:

- Lower your credit score

- Close existing accounts

- Affect current loans

- Prevent you from making purchases with existing credit cards

- Stop creditors from reporting account activity

- Change your payment history

Your current financial accounts continue operating exactly as they did before the freeze was placed.

Why People Confuse Credit Freezes With Credit Problems

The confusion often comes from the fact that a credit freeze can temporarily interfere with new credit applications.

For example, if you apply for:

- A mortgage

- A car loan

- A personal loan

- A new credit card

The lender may be unable to access your credit report until you temporarily lift the freeze.

This can delay an application, but it does not lower your credit score or create negative marks on your credit report.

Can You Still Build Credit With a Freeze?

Yes.

Even after completing how to freeze your credit after identity theft, you can continue building credit through responsible use of your existing accounts.

Your credit score can still improve if you:

- Make payments on time

- Keep credit card balances low

- Maintain long-standing accounts

- Avoid missed payments

- Manage debt responsibly

The freeze only restricts access to your credit file—it does not stop positive account activity from being reported.

Why a Credit Freeze Is Often Worth It

For many identity theft victims, the protection offered by a credit freeze far outweighs any inconvenience associated with temporarily lifting it for future applications.

After identity theft, preventing criminals from opening new accounts in your name becomes a much higher priority than maintaining immediate access to new credit.

That’s why consumer protection experts frequently recommend how to freeze your credit after identity theft as one of the most effective defenses against new account fraud.

Additional Protection Beyond a Credit Freeze

While a credit freeze helps prevent unauthorized credit applications, it does not actively monitor your identity. Learn What Happens After a Data Breach and why stolen information can continue circulating long after the initial exposure.

Many consumers choose to combine a credit freeze with:

- Credit monitoring

- Identity monitoring

- Dark web monitoring

- Fraud alerts

- Account activity notifications

Aura is one of the most popular options, and our detailed Aura review explains its monitoring and recovery features.

The bottom line is simple: how to freeze your credit after identity theft is a powerful security step that can help prevent future fraud, and it will not hurt your credit score. Your credit can continue to grow and improve while your credit report remains protected from unauthorized access.

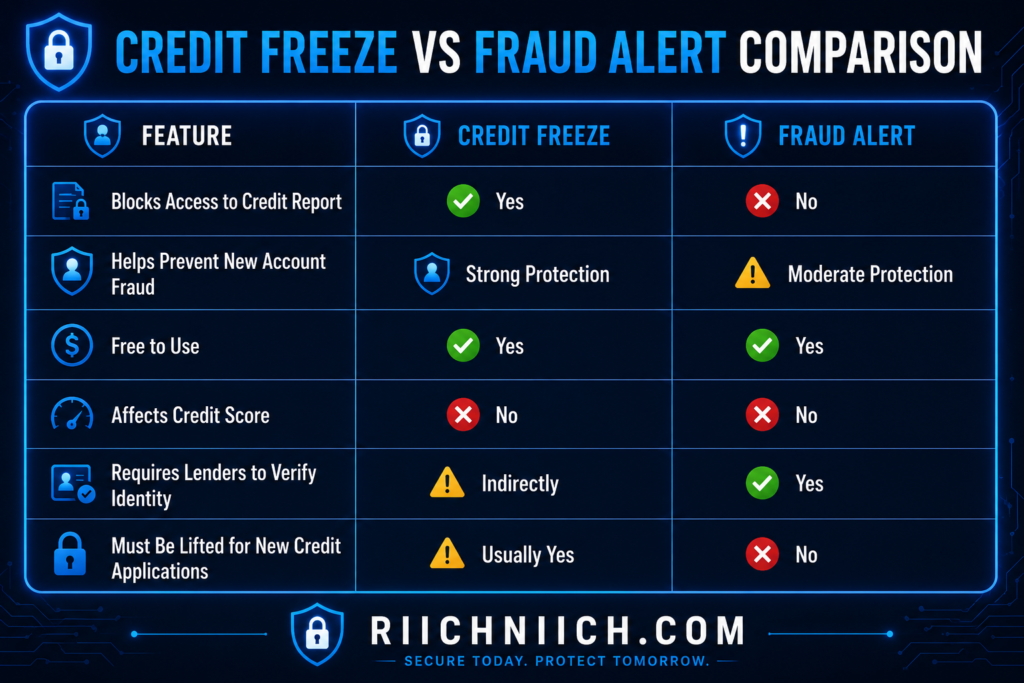

Credit Freeze vs Fraud Alert: Which Is Better After Identity Theft?

When researching how to freeze your credit after identity theft, you’ll often come across another option called a fraud alert. While both tools are designed to help protect your credit, they work very differently and offer different levels of protection.

Understanding the differences between a credit freeze and a fraud alert can help you choose the best solution for your situation after identity theft.

What Is a Credit Freeze?

A credit freeze, also called a security freeze, restricts access to your credit report. Most lenders cannot view your credit file while the freeze is active, making it much more difficult for identity thieves to open new accounts in your name.

A credit freeze:

- Restricts access to your credit report

- Helps prevent new account fraud

- Is free to place and remove

- Remains active until you lift or remove it

- Does not affect your credit score

Many experts consider a credit freeze to be the strongest protection available after identity theft.

What Is a Fraud Alert?

A fraud alert places a warning on your credit report that tells lenders to take extra steps to verify your identity before approving new credit.

Unlike a credit freeze, a fraud alert does not block access to your credit report. Instead, it encourages creditors to verify that the person applying for credit is actually you.

A fraud alert:

- Allows lenders to access your credit report

- Requests additional identity verification

- Is easier to set up

- May provide less protection than a credit freeze

- Does not affect your credit score

Credit Freeze vs Fraud Alert Comparison

Which Option Is Better After Identity Theft?

For most victims, a credit freeze offers stronger protection. For a deeper comparison, see our complete guide on Credit Freeze vs Credit Lock and how each option protects your credit file.

If someone has already stolen your personal information, learning how to freeze your credit after identity theft can create a more effective barrier against future fraud because lenders generally cannot review your credit report while the freeze remains active.

A fraud alert can still be useful, but it relies on lenders to follow verification procedures. A credit freeze places stricter restrictions on access to your credit file.

Can You Use Both?

Yes.

Many identity theft victims choose to combine a credit freeze with a fraud alert for additional protection.

Using both may help:

- Reduce the risk of unauthorized credit applications

- Increase identity verification requirements

- Strengthen your identity theft recovery efforts

- Add multiple layers of protection

What About Credit Monitoring?

While both fraud alerts and credit freezes help protect your credit report, neither option actively monitors your identity.

This is an important distinction when considering how to freeze your credit after identity theft.

Neither a credit freeze nor a fraud alert will notify you if:

- Your Social Security number appears on the dark web

- Your information is exposed in a future data breach

- Existing accounts are compromised

- Criminals attempt account takeovers

For this reason, many identity theft victims supplement a credit freeze with identity monitoring and credit monitoring services that provide real-time alerts and fraud detection.

The Bottom Line

If you’re deciding between a fraud alert and a credit freeze after identity theft, a credit freeze generally provides stronger protection against new account fraud.

A fraud alert can add another layer of security, but it does not prevent lenders from accessing your credit report. Because of this, most experts recommend prioritizing how to freeze your credit after identity theft as one of the first recovery steps after discovering identity theft.

By understanding the strengths and limitations of both options, you can make a more informed decision about protecting your credit and reducing the risk of future identity theft.

Additional Steps to Take After Freezing Your Credit

Completing how to freeze your credit after identity theft is one of the most important actions you can take, but it should not be the only step in your recovery plan. A credit freeze helps prevent new account fraud, but identity thieves may still attempt to misuse your personal information in other ways.

To fully protect yourself, it’s important to take additional measures that strengthen your financial security and help you detect future threats.

Review Your Credit Reports Regularly

Even after freezing your credit, you should continue monitoring your credit reports for suspicious activity.

Watch for:

- Accounts you don’t recognize

- Unauthorized hard inquiries

- Incorrect personal information

- Collection accounts that aren’t yours

- Signs of new identity theft attempts

Regular reviews can help you identify problems before they become larger financial issues.

Change Passwords on Important Accounts

If your identity theft resulted from a data breach, phishing attack, or compromised account, changing passwords should be a top priority.

Update passwords for:

- Email accounts

- Banking accounts

- Credit card accounts

- Shopping websites

- Investment accounts

- Password manager accounts

Use strong, unique passwords for every account and avoid reusing passwords across multiple websites.

Enable Multi-Factor Authentication

Multi-factor authentication (MFA) adds an extra layer of protection by requiring a second verification step when logging in.

Even if a criminal obtains your password, MFA can help prevent unauthorized access to your accounts.

Enable MFA on:

- Email accounts

- Financial accounts

- Social media profiles

- Password managers

- Cloud storage accounts

This simple security measure can significantly reduce the risk of account takeover attacks.

Monitor Your Financial Accounts

A credit freeze does not monitor your existing bank accounts or credit cards.

Continue checking:

- Credit card transactions

- Bank account activity

- Loan statements

- Investment accounts

- Payment app activity

Report suspicious transactions immediately to the financial institution involved.

Watch for Future Data Breaches

If your information has already been exposed once, ongoing monitoring becomes even more important. 👉 Aura continuously monitors for identity theft risks and alerts you when your personal information appears in places it shouldn’t.

Unfortunately, stolen personal information may continue circulating online long after the original incident.

Even after completing how to freeze your credit after identity theft, your information could appear in future data breaches, criminal marketplaces, or dark web forums.

This is one reason many consumers choose to monitor their personal information and receive alerts when exposure is detected.

Consider Identity Theft Protection Services

A credit freeze helps stop new credit applications, but it does not provide real-time alerts about identity-related threats.

Many identity theft protection services offer:

- Credit monitoring

- Dark web monitoring

- Identity monitoring alerts

- Fraud detection

- Identity restoration assistance

For individuals recovering from identity theft, these tools can provide additional visibility into potential risks and help detect suspicious activity more quickly.

Keep Records of Your Recovery Efforts

If identity theft has already occurred, maintain documentation related to:

- Credit freeze confirmations

- Fraud reports

- Identity theft reports

- Dispute letters

- Communication with financial institutions

- Credit bureau correspondence

Keeping organized records can make future disputes and recovery efforts much easier.

Stay Alert for Phishing Scams

Identity thieves often target victims repeatedly. After a data breach or identity theft incident, scammers may attempt to gather even more information through fraudulent emails, text messages, or phone calls.

Be cautious of:

- Urgent requests for personal information

- Unexpected account verification messages

- Suspicious links

- Fake financial institution emails

- Calls requesting Social Security numbers

Avoid clicking unknown links and verify communications directly with the organization involved.

While how to freeze your credit after identity theft is one of the strongest defenses against new account fraud, combining it with good security habits, ongoing monitoring, and identity protection tools can provide a much more complete defense against future identity theft attempts.

How Identity Theft Protection Services Can Help Monitor Your Credit

Completing how to freeze your credit after identity theft is one of the most effective ways to prevent criminals from opening new accounts in your name. However, a credit freeze only addresses one part of the identity theft problem.

A credit freeze does not actively monitor your personal information, track suspicious activity, or alert you when new threats appear. This is where identity theft protection services can provide additional value.

Identity theft protection services help monitor your credit, personal information, and online exposure so you can identify potential problems before they become major financial issues. You can compare the leading providers in our guide to the Best Identity Theft Protection Services.

Why a Credit Freeze Isn’t Always Enough

Many people assume that once they complete how to freeze your credit after identity theft, they’re fully protected. While a credit freeze significantly reduces the risk of new account fraud, it cannot detect every type of identity theft.

For example, a credit freeze generally will not notify you if:

- Your Social Security number appears on the dark web

- Someone attempts to take over an existing account

- Your personal information is exposed in a future data breach

- Fraudulent activity occurs on current financial accounts

- Criminals use your information for non-credit-related fraud

Because identity theft can take many forms, ongoing monitoring can provide an additional layer of protection.

What Identity Theft Protection Services Monitor

Most identity theft protection services monitor a variety of risk indicators, including:

- Credit report changes

- New account activity

- Hard credit inquiries

- Dark web exposure

- Social Security number misuse

- Personal information leaks

- Data breach notifications

- Identity fraud alerts

These services are designed to notify you quickly when suspicious activity occurs so you can take action before significant damage is done.

Credit Monitoring Alerts Can Help You Act Faster

One of the biggest advantages of identity theft protection services is real-time monitoring.

Instead of manually checking your credit reports every few weeks, you may receive alerts when:

- A new account is opened

- A lender performs a hard inquiry

- Personal information appears in criminal databases

- Significant credit file changes occur

Early detection often gives victims more time to respond before fraud escalates.

Identity Restoration Assistance

Some identity theft protection providers also offer identity restoration services.

If identity theft occurs, specialists may help with:

- Fraud reports

- Credit bureau disputes

- Recovery documentation

- Account restoration

- Identity theft resolution

For victims facing multiple fraudulent accounts or extensive damage, this support can save significant time and frustration.

Combining Credit Freezes and Identity Monitoring

The strongest protection often comes from combining multiple security measures.

Many consumers use:

- Credit freezes

- Credit monitoring

- Identity monitoring

- Dark web monitoring

- Multi-factor authentication

- Strong password management

When used together, these tools can provide broader protection than any single solution alone.

This is especially important after completing how to freeze your credit after identity theft, because identity thieves may continue targeting your information long after the original incident.

Who Should Consider Identity Theft Protection?

Identity theft protection services may be especially useful if:

- You’ve already experienced identity theft

- Your information was exposed in a data breach

- Your Social Security number was compromised

- You want ongoing fraud monitoring

- You prefer proactive alerts rather than manual monitoring

For many people, the added visibility and early-warning capabilities provide valuable peace of mind.

The Bottom Line

Learning how to freeze your credit after identity theft is one of the most important recovery steps you can take, but a credit freeze alone cannot monitor your identity or alert you to new threats.

Identity theft protection services help fill those gaps by providing ongoing monitoring, fraud alerts, dark web surveillance, and identity recovery assistance. When combined with a credit freeze, they can create a stronger defense against future identity theft attempts.

Common Mistakes to Avoid When Freezing Your Credit

Learning how to freeze your credit after identity theft is an important step toward protecting yourself from fraud, but many people make mistakes that can reduce the effectiveness of a credit freeze. Understanding these common errors can help ensure you get the maximum protection from your security freeze.

A credit freeze is one of the strongest tools available for preventing new account fraud, but only when it’s used correctly.

Mistake #1: Freezing Only One Credit Bureau

One of the most common mistakes is freezing your credit with only one bureau.

Remember that lenders may use:

- Equifax

- Experian

- TransUnion

If you only freeze one credit report, identity thieves may still be able to exploit the others.

To fully complete how to freeze your credit after identity theft, you should place a credit freeze with all three major credit bureaus.

Mistake #2: Assuming a Credit Freeze Monitors Your Identity

A credit freeze restricts access to your credit report, but it does not actively monitor your identity.

Many people incorrectly assume they will receive alerts if:

- Their Social Security number appears on the dark web

- Personal information is exposed in a data breach

- Existing accounts are compromised

- Fraudulent transactions occur

Learning How to Protect Yourself from Identity Theft can help you build additional layers of security beyond a credit freeze.

A credit freeze helps prevent new account fraud, but it does not replace credit monitoring or identity monitoring.

Mistake #3: Forgetting Login Credentials and Recovery Information

After placing a credit freeze, you’ll receive account access details from each bureau.

Losing these credentials can create frustration later if you need to:

- Temporarily lift a credit freeze

- Apply for a mortgage

- Open a new credit card

- Finance a vehicle

- Remove the freeze

Store your login information securely so it’s easy to access when needed.

Mistake #4: Ignoring Existing Accounts

Another common mistake is focusing only on new account fraud while ignoring current financial accounts.

Even after completing how to freeze your credit after identity theft, criminals may still attempt to access:

- Existing credit cards

- Bank accounts

- Investment accounts

- Payment apps

- Online financial services

Continue monitoring account activity regularly for suspicious transactions.

Mistake #5: Delaying Action After Identity Theft

Some victims wait days or even weeks before placing a credit freeze.

Unfortunately, identity thieves often act quickly once they obtain personal information. Delaying a security freeze can provide additional opportunities for fraud.

If you suspect identity theft, learning how to freeze your credit after identity theft and acting promptly can significantly reduce the risk of further damage.

Mistake #6: Not Reviewing Credit Reports

A credit freeze does not automatically correct fraudulent accounts that already exist.

You should still review your credit reports for:

- Unauthorized accounts

- Suspicious inquiries

- Incorrect information

- Collection accounts

- Signs of identity theft

Regular credit report reviews remain an important part of your recovery strategy.

Mistake #7: Forgetting to Lift the Freeze Before Applying for Credit

Many consumers successfully freeze their credit but forget about it when applying for a loan or credit card later.

This can lead to:

- Delayed approvals

- Application denials

- Frustration during the lending process

Before applying for new credit, verify whether the lender requires access to your credit report and temporarily lift the freeze if necessary.

Mistake #8: Relying Solely on a Credit Freeze

A credit freeze is powerful, but it should be part of a broader security strategy.

Additional protections may include:

- Strong passwords

- Multi-factor authentication

- Identity monitoring

- Credit monitoring

- Dark web monitoring

- Account alerts

If you’re wondering whether these services are worth paying for, read our guide, ‘Is Identity Theft Protection Worth It?’

The Bottom Line

Understanding how to freeze your credit after identity theft is only part of the process. Avoiding common mistakes can help ensure your credit freeze works as intended and provides the strongest possible protection.

By freezing all three credit reports, monitoring your accounts, protecting your credentials, and staying alert for future threats, you’ll be in a much stronger position to defend yourself against identity theft.

Frequently Asked Questions About Freezing Your Credit After Identity Theft

How long does it take to freeze your credit?

One of the most common questions about how to freeze your credit after identity theft is how quickly the process works.

In most cases, online credit freezes can be completed within minutes. Once your identity is verified, the freeze is typically activated shortly afterward. Phone and mail requests may take longer depending on processing times.

Does freezing your credit cost money?

No. Federal law allows consumers to place, temporarily lift, and remove credit freezes for free.

There is no charge to freeze your credit report with:

- Equifax

- Experian

- TransUnion

Because the process is free, it’s often one of the most effective and affordable ways to protect yourself after identity theft.

Do I need to freeze all three credit reports?

Yes.

To fully complete how to freeze your credit after identity theft, you should place a credit freeze with all three major credit bureaus.

Freezing only one or two credit reports may leave gaps that identity thieves could potentially exploit if a lender uses an unfrozen bureau during the application process.

Can I still use my credit cards after freezing my credit?

Yes.

A credit freeze only restricts access to your credit report for new credit applications. It does not affect your existing accounts.

You can continue using:

- Credit cards

- Bank accounts

- Mortgages

- Auto loans

- Existing lines of credit

Normal account activity continues uninterrupted.

Does a credit freeze affect my credit score?

No.

A credit freeze does not:

- Lower your credit score

- Impact your credit history

- Affect your payment history

- Change your credit utilization

Your credit score will continue to be calculated normally while the freeze remains active.

Can I temporarily lift a credit freeze?

Yes.

If you need to apply for a mortgage, auto loan, apartment lease, or credit card, you can temporarily lift your freeze.

Most credit bureaus allow you to:

- Lift the freeze for a specific lender

- Temporarily unfreeze your credit report

- Remove the freeze permanently

This flexibility allows you to maintain protection while still accessing credit when needed.

How long should I keep my credit frozen?

Many identity theft victims keep their credit freeze in place indefinitely.

Since a credit freeze is free and does not affect your credit score, there is often little downside to maintaining the freeze until you need access to new credit.

The right decision depends on your personal situation and level of risk.

Does a credit freeze stop identity theft completely?

No.

Although how to freeze your credit after identity theft is one of the strongest defenses against new account fraud, it does not prevent every type of identity theft.

A credit freeze cannot stop:

- Account takeover fraud

- Unauthorized bank transactions

- Tax identity theft

- Medical identity theft

- Dark web exposure

- Existing account fraud

This is why many consumers combine a credit freeze with identity monitoring and credit monitoring services.

Is a credit freeze better than a fraud alert?

For most identity theft victims, a credit freeze offers stronger protection because it restricts access to your credit report rather than simply warning lenders to verify your identity.

However, some consumers choose to use both a fraud alert and a credit freeze for additional security.

What should I do if my information is exposed in a data breach?

If your personal information is exposed, experts often recommend:

- Reviewing your credit reports

- Monitoring financial accounts

- Changing passwords

- Enabling multi-factor authentication

- Completing how to freeze your credit after identity theft

- Considering identity theft protection services

Taking action quickly can reduce the risk of additional fraud.

Should I use identity theft protection services after freezing my credit?

Many consumers choose to do so.

A credit freeze helps prevent new account fraud, but identity theft protection services may also provide:

- Credit monitoring

- Dark web monitoring

- Fraud alerts

- Identity monitoring

- Identity restoration assistance

These services can help identify threats that a credit freeze alone may not detect.

Understanding how to freeze your credit after identity theft can help you make informed decisions about protecting your financial future and reducing the risk of further fraud.

Final Verdict: How to Freeze Your Credit After Identity Theft

If you’ve become a victim of identity theft, learning how to freeze your credit after identity theft is one of the most important actions you can take to protect your financial future.

A credit freeze helps prevent criminals from opening new credit cards, loans, and other accounts in your name by restricting access to your credit reports. If you’ve already experienced fraud, follow these steps on What To Do Immediately if Your identity is Stolen to begin the recovery process. Best of all, it is free, does not hurt your credit score, and can be completed in a relatively short amount of time.

However, while a credit freeze provides strong protection against new account fraud, it is not a complete identity theft solution. Identity thieves may still attempt to misuse your personal information through existing accounts, phishing attacks, account takeovers, or future data breaches.

That’s why many security experts recommend combining how to freeze your credit after identity theft with additional protective measures such as:

- Credit monitoring

- Identity monitoring

- Dark web monitoring

- Multi-factor authentication

- Strong password management

- Regular credit report reviews

For many people, identity theft protection services can provide valuable peace of mind by monitoring for suspicious activity and alerting you to potential threats before they become major problems. While a credit freeze helps block unauthorized credit applications, monitoring services can help detect risks that a freeze alone cannot identify.

If your personal information was exposed in a data breach or if you’ve already experienced identity theft, taking a proactive approach can significantly reduce the risk of future fraud.

Key Takeaways

Before you finish, remember these important points:

- Place a credit freeze with Equifax, Experian, and TransUnion.

- A credit freeze does not affect your credit score.

- Existing accounts continue to work normally.

- A credit freeze helps prevent new account fraud.

- Ongoing monitoring can provide additional protection.

- Acting quickly after identity theft may help minimize financial damage.

Ultimately, how to freeze your credit after identity theft is one of the most effective and affordable tools available for protecting yourself after your personal information has been compromised. When combined with strong security habits and identity monitoring, it can help you regain control of your finances and reduce the likelihood of becoming a victim again.

If you’re serious about protecting your identity after a breach or fraud incident, taking action today is far better than waiting until another fraudulent account appears in your name.