Do You Really Need Identity Theft Protection in 2026? With data breaches increasing, phishing scams evolving, and more of our financial lives moving online, it’s a fair — and important — question.

Some people rely on free credit monitoring and frozen credit reports. Others choose paid identity theft protection for broader monitoring and recovery support. The right answer depends on your risk level, digital habits, and how much responsibility you’re willing to handle if fraud happens.

In this guide, we’ll break down how identity theft really happens, what protection services actually cover, the real costs of fraud, and whether the monthly fee makes sense for your situation — so you can make a confident, informed decision.

🔥 Quick Answer: Do You Really Need Identity Theft Protection?

No — you don’t *technically* need identity theft protection.

But most people choose it because monitoring everything manually is time-consuming and easy to miss.

Identity theft can happen quickly, and the sooner you detect it, the less damage it causes.

👉 See how Aura simplifies identity protection!

Table of Contents

What Identity Theft Protection Actually Covers (And What It Doesn’t)

If you’re asking, “Do You Really Need Identity Theft Protection in 2026?”, the first thing you need to understand is what these services actually do — and just as importantly — what they don’t do.

There’s a lot of confusion in this space. Some people believe identity theft protection prevents fraud completely. Others think it’s just credit monitoring with a fancy name.

The truth is somewhere in the middle.

Let’s break it down clearly.

Identity Theft Protection: DIY vs Paid Services

You can protect yourself without paying for a service — but it requires consistent effort.

Do-It-Yourself Protection (Free)

✔ Check credit reports regularly

✔ Monitor bank accounts

✔ Freeze your credit manually

✔ Watch for suspicious activity

Paid Protection (Automated)

✔ Continuous monitoring

✔ Real-time alerts

✔ Identity recovery support

✔ Insurance coverage

The biggest difference is automation vs manual effort.

👉 Compare Aura’s automated protection here!

✅ What Identity Theft Protection Actually Covers

Most reputable identity theft protection services include the following core features:

1️⃣ Credit Monitoring (Often 1 or 3 Bureaus)

These services monitor your credit file at one or all three major bureaus:

- Experian

- Equifax

- TransUnion

If a new credit inquiry, account opening, or suspicious change appears, you receive an alert.

However, credit monitoring only detects activity after it hits your credit report.

External resource: The Federal Trade Commission explains how credit monitoring works and why it doesn’t stop fraud before it happens.

2️⃣ Dark Web Monitoring

This is where full identity theft protection goes beyond free credit tools.

Dark web monitoring scans underground forums and data leak markets for:

- Your Social Security number

- Email addresses

- Passwords

- Bank account numbers

If your personal data appears in a breach, you’re alerted early — often before financial damage occurs.

External resource: Identity Theft Resource Center regularly tracks data breaches and reports how stolen data circulates online.

3️⃣ Identity Restoration Support

This is one of the biggest differences between free monitoring and paid protection.

If your identity is stolen, many services assign you a fraud resolution specialist who helps:

- Contact creditors

- File disputes

- Submit fraud affidavits

- Work with financial institutions

- Restore your identity

The Federal Trade Commission provides DIY recovery steps at IdentityTheft.gov — but having a specialist can significantly reduce stress and time spent.

For many people, this support alone answers the question:

Do You Really Need Identity Theft Protection in 2026?

If you value having expert help during a crisis, this feature matters.

4️⃣ Identity Theft Insurance

Most major services include insurance coverage, often up to $1 million.

Important clarification:

Insurance does not reimburse stolen money directly in most cases. Instead, it covers:

- Legal fees

- Lost wages

- Notary costs

- Certified mail

- Document replacement

External resource: The National Association of Insurance Commissioners explains how identity theft insurance policies are structured.

This protection is more about recovery expenses than replacing funds.

❌ What Identity Theft Protection Does Not Cover

Now for the part many sales pages gloss over.

Understanding limitations builds trust — and helps you decide whether you truly need it.

1️⃣ It Does NOT Prevent All Fraud

No service can stop someone from attempting fraud.

What it does is detect activity faster and help you recover more efficiently.

If someone steals your debit card and uses it immediately, your bank’s fraud department may catch it before your monitoring service does.

2️⃣ It Does NOT Replace Smart Security Habits

You still need to:

- Use strong passwords

- Enable two-factor authentication

- Avoid suspicious links

- Freeze your credit if needed

Even the best monitoring service can’t fix unsafe online behavior.

External resource: The Cybersecurity and Infrastructure Security Agency provides free cybersecurity best practices for individuals.

3️⃣ It Does NOT Guarantee Zero Financial Loss

While alerts can be fast, financial institutions ultimately control reimbursement policies.

Most credit card fraud is covered by federal law under the Fair Credit Billing Act — even without identity theft protection.

That’s why some people conclude they may not need paid protection — depending on their risk tolerance.

So… Do You Really Need Identity Theft Protection in 2026?

Here’s the honest answer:

It depends on your situation.

You may want identity theft protection if:

- You manage multiple family members’ identities

- You’ve been part of a previous data breach

- You frequently shop or bank online

- You don’t want to handle recovery alone

You may not need it if:

- You actively freeze your credit

- You manually monitor accounts daily

- You’re comfortable managing disputes independently

The key distinction is this:

👉 Free tools alert you.

👉 Paid services monitor broader data sources and assist with recovery.

Services like NordProtect provide identity monitoring, alerts, and recovery support, making them a strong option for those who want comprehensive protection.

If peace of mind and guided recovery matter to you, identity theft protection can be a rational investment — not just a fear-based purchase.

Understanding exactly what’s covered — and what isn’t — helps you answer the bigger question confidently:

Do You Really Need Identity Theft Protection in 2026?

The next section will help you compare free credit monitoring and full-service protection side-by-side so you can make a fully informed decision.

How Identity Theft Really Happens in 2026

If you’re still wondering, Do You Really Need Identity Theft Protection in 2026?, it helps to understand how identity theft actually happens today.

Most people picture a hacker in a dark room breaking into their bank account.

That’s rarely how it works.

In 2026, identity theft is usually the result of data breaches, automation, and human error — not cinematic hacking scenes.

Let’s break down the real-world methods criminals use.

1️⃣ Massive Data Breaches (The Biggest Source of Stolen Data)

The majority of identity theft starts with large-scale corporate data breaches.

When companies store customer information — emails, passwords, Social Security numbers, dates of birth — that data becomes a target.

Organizations like the Identity Theft Resource Center report hundreds to thousands of breaches every year, exposing millions of records.

Once breached, this information is:

- Sold in bulk

- Bundled into identity “packages”

- Traded on underground forums

You may never know your data was exposed until fraud occurs.

Resource: 2025 Data Breach Report

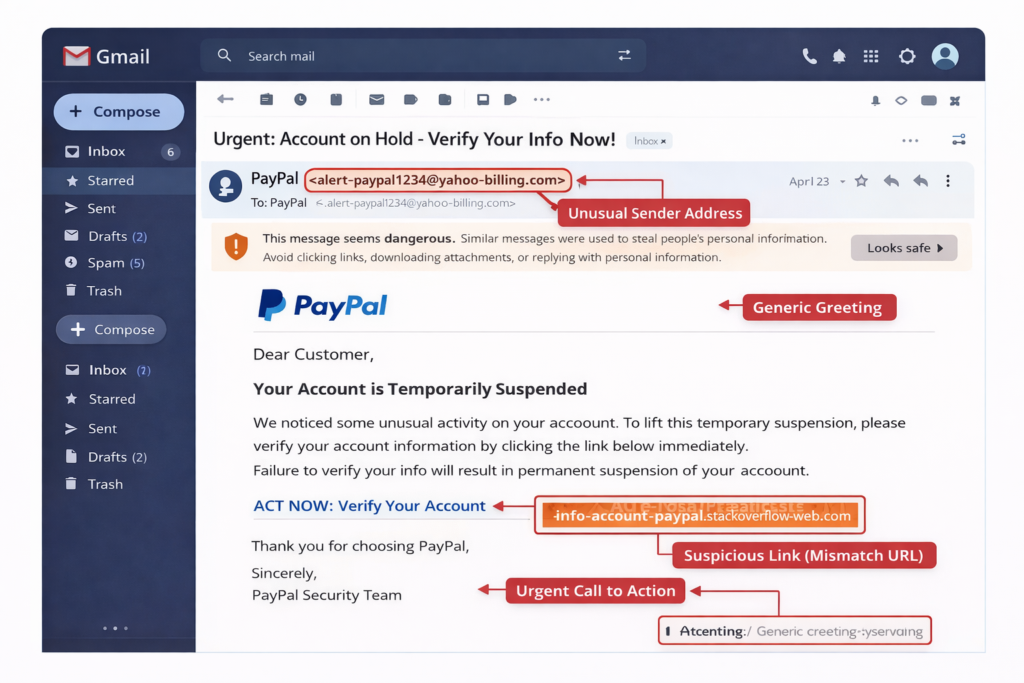

2️⃣ Phishing & Social Engineering Attacks

Phishing remains one of the fastest-growing methods of identity theft.

Criminals send emails or texts that look legitimate — from banks, delivery companies, or even government agencies.

The Federal Trade Commission regularly warns that phishing scams continue to increase because they exploit human behavior rather than technology flaws.

Examples include:

- Fake package delivery notifications

- “Suspicious login” emails

- IRS or Social Security impersonation calls

- Text messages asking you to “verify” account details

Once you click and enter information, attackers gain direct access.

3️⃣ Credential Stuffing (Using Your Old Passwords Against You)

Here’s something most people don’t realize:

If you reuse passwords, you dramatically increase your risk.

When one website is breached, criminals test those same login credentials across:

- Banks

- Retail sites

- Payment apps

- Crypto exchanges

This automated method is called credential stuffing.

According to the Cybersecurity and Infrastructure Security Agency, password reuse is one of the most common security vulnerabilities among consumers.

This is why identity theft in 2026 often feels sudden — but actually began months earlier with an unrelated breach.

4️⃣ SIM Swapping & Mobile Account Takeovers

As mobile banking grows, criminals increasingly target phone numbers.

SIM swapping happens when someone convinces a carrier to transfer your number to their device.

Once they control your number, they can:

- Intercept two-factor authentication codes

- Reset banking passwords

- Access financial apps

This type of fraud has grown alongside cryptocurrency and digital banking platforms.

External resource: The Federal Bureau of Investigation has issued public warnings about SIM swap fraud.

5️⃣ Public WiFi & Unsecured Networks

Public WiFi networks — airports, coffee shops, hotels — are convenient but risky.

Attackers can:

- Create fake hotspot networks

- Intercept unencrypted traffic

- Launch “man-in-the-middle” attacks

If you log into financial accounts on unsecured WiFi without protection, your data can be exposed.

While encryption has improved, unsecured browsing still presents risk.

6️⃣ Synthetic Identity Fraud

One of the fastest-growing fraud types in 2026 is synthetic identity fraud.

This happens when criminals combine:

- A real Social Security number (often from a child or senior)

- A fake name

- A fake birth date

They slowly build credit under this identity before committing large-scale fraud.

This type of theft can go undetected for years — especially affecting minors and older adults.

The Federal Reserve has published research on synthetic identity fraud as one of the most complex financial crime trends.

The Pattern Behind Modern Identity Theft

Notice something?

Most identity theft in 2026 is:

- Automated

- Data-driven

- Scalable

- Often invisible until damage occurs

It rarely starts with someone targeting you personally.

It starts with exposed data circulating quietly.

This brings us back to the core question:

Do You Really Need Identity Theft Protection in 2026?

If identity theft is primarily driven by:

- Data breaches outside your control

- Password leaks from old accounts

- Advanced fraud methods like synthetic identities

Then monitoring and early detection may provide more value than many people assume.

The decision isn’t about fear.

It’s about understanding how modern identity theft works — and deciding whether you want alerts and recovery support if your information surfaces in one of these scenarios.

In the next section, we’ll compare identity theft protection with free credit monitoring so you can evaluate whether basic tools are enough — or if broader monitoring makes more sense for your situation.

Identity Theft Protection vs Free Credit Monitoring: What’s the Difference?

If you’re asking, Do You Really Need Identity Theft Protection in 2026?, this is the section that usually determines the answer.

Many people assume free credit monitoring and identity theft protection are basically the same.

They are not.

They serve different purposes, detect different risks, and provide very different levels of support.

Let’s break it down clearly.

What Free Credit Monitoring Actually Does

Free credit monitoring services track changes to your credit report.

This typically includes:

- New credit inquiries

- New accounts opened in your name

- Changes to your credit score

- Address updates

You can access free weekly credit reports through AnnualCreditReport.com, which is authorized by federal law.

The Federal Trade Commission explains that credit monitoring alerts you after activity appears on your credit file.

That’s the key limitation.

If someone opens a fraudulent credit card, you’ll get notified — but only once it’s already happened.

What Identity Theft Protection Covers Beyond Credit Reports

Identity theft protection includes credit monitoring — but expands far beyond it.

Depending on the provider, services may include:

- Dark web monitoring

- Social Security number tracking

- Bank account monitoring

- Investment account monitoring

- Home title monitoring

- Identity restoration specialists

- Insurance coverage

The difference is scope.

Credit monitoring watches your credit file.

Identity protection monitors your personal data ecosystem.

The Cybersecurity and Infrastructure Security Agency highlights that modern identity theft often starts outside the credit system — including account takeovers and leaked credentials.

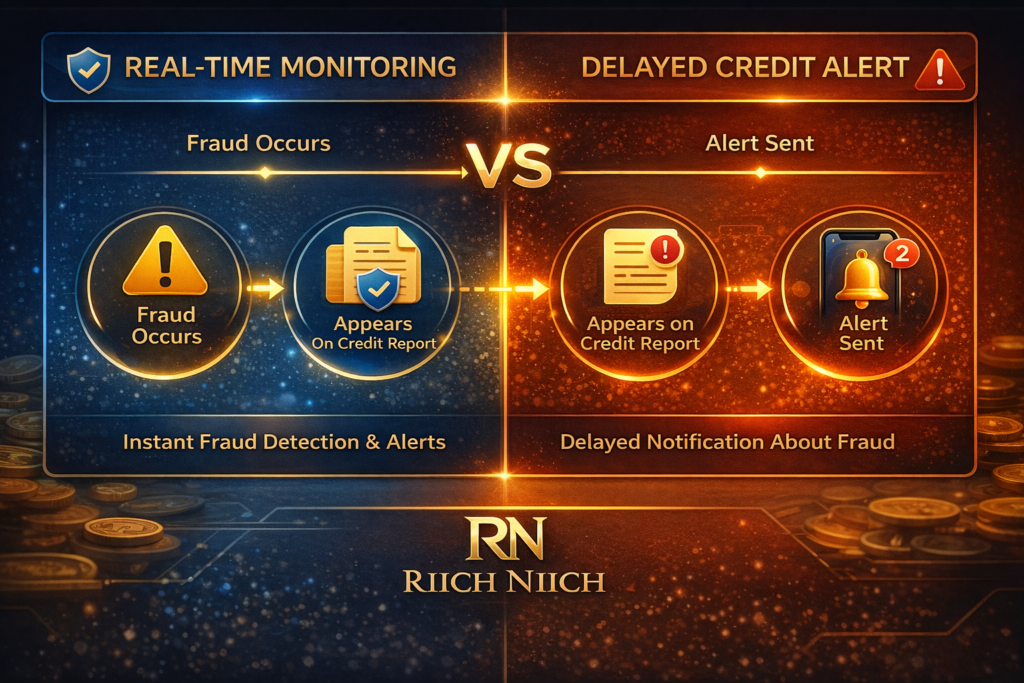

Speed of Detection: Reactive vs Broader Monitoring

Free credit monitoring is reactive.

It alerts you once financial damage reaches your credit file.

Identity theft protection may detect:

- Your SSN appearing in a breach

- Stolen passwords circulating online

- Suspicious bank account changes

- Address change attempts

Earlier alerts can mean faster response — which may reduce financial and administrative damage.

The Identity Theft Resource Center reports that early detection significantly lowers the recovery burden for victims.

Recovery Help: The Biggest Difference

This is where the gap becomes clear.

Free credit monitoring:

- Sends alerts

- Leaves recovery entirely up to you

Identity theft protection:

- Assigns a fraud resolution specialist

- Helps contact creditors

- Guides dispute filings

- Assists with documentation

- Provides insurance coverage for eligible recovery expenses

The Federal Trade Commission offers DIY recovery tools at IdentityTheft.gov — but many people underestimate how time-consuming this process can be.

If you value having a professional handle the paperwork and calls, this feature alone may justify the cost.

Cost Comparison

Free credit monitoring:

- $0

- Limited to credit file alerts

Identity theft protection:

- Typically $10–$30 per month

- Broader monitoring

- Recovery support

- Insurance

The real question isn’t just cost.

It’s risk tolerance.

Are you comfortable managing identity recovery alone if something goes wrong?

Or would you prefer guided support?

So… Do You Really Need Identity Theft Protection in 2026?

Here’s the honest breakdown:

You might be fine with free credit monitoring if:

- You regularly freeze your credit

- You monitor bank accounts daily

- You’re comfortable filing disputes yourself

- You have minimal digital exposure

Identity theft protection may make sense if:

- You manage multiple identities (family members)

- You’ve experienced a previous breach

- You prefer early alerts beyond credit reports

- You want recovery assistance if fraud occurs

Free monitoring answers the question:

“Has fraud already affected my credit?”

Identity protection answers the question:

“Is my personal data circulating somewhere it shouldn’t be — and who helps me fix it?”

That distinction is what ultimately helps you decide:

For those who want paid protection without a high monthly cost, services like IdentityIQ offer a more affordable entry point into identity monitoring.

Do You Really Need Identity Theft Protection in 2026?

In the next section, we’ll examine the real financial and emotional costs of identity theft — so you can weigh the monthly fee against the potential impact of fraud.

The Real Costs of Identity Theft (Financial and Emotional)

If you’re seriously asking, Do You Really Need Identity Theft Protection in 2026?, you need to understand the true cost of identity theft.

Not just the headline numbers.

Not just “fraud happens.”

But the real financial damage, time lost, and emotional stress victims experience.

Because the decision often comes down to this:

Is the monthly cost of protection worth avoiding the potential fallout?

Let’s break it down clearly.

1️⃣ Direct Financial Losses

Identity theft can result in:

- Fraudulent credit card charges

- Unauthorized bank withdrawals

- New loans opened in your name

- Tax refund fraud

- Medical identity theft

According to the Federal Trade Commission, consumers report billions of dollars in fraud losses annually in the United States.

While many banks reimburse fraudulent credit card charges, reimbursement is not always immediate — and debit card fraud can temporarily freeze access to your money.

That delay alone can cause serious disruption.

2️⃣ Lost Time and Administrative Burden

Money is only part of the cost.

The Identity Theft Resource Center reports that victims often spend weeks or months resolving identity theft cases.

Recovery may involve:

- Filing fraud affidavits

- Contacting creditors repeatedly

- Disputing credit report inaccuracies

- Replacing identification documents

- Monitoring accounts long-term

Some cases require dozens of phone calls and written disputes.

Even if financial losses are reimbursed, the time lost is not.

3️⃣ Credit Score Damage

If fraudulent accounts go unnoticed, they can significantly lower your credit score.

That can affect:

- Mortgage approval

- Auto loan interest rates

- Apartment rental applications

- Insurance premiums

The Consumer Financial Protection Bureau explains that inaccurate information on a credit report can impact lending decisions until corrected.

Restoring your credit file can take months — sometimes longer.

This is one reason early detection matters.

4️⃣ Emotional Stress and Anxiety

This is the part most people underestimate.

Victims often report:

- Ongoing anxiety about accounts

- Sleep disruption

- Fear of future fraud

- Loss of trust in online systems

According to victim impact surveys published by the Identity Theft Resource Center, emotional distress can persist long after financial recovery.

The psychological toll is real.

When your identity is misused, it feels personal.

5️⃣ Opportunity Costs

There’s another hidden cost: distraction.

When dealing with fraud, you may:

- Miss work

- Delay major purchases

- Postpone financial decisions

- Spend hours monitoring accounts

Time spent fixing identity theft is time not spent building wealth or focusing on your family.

That opportunity cost rarely gets mentioned — but it matters.

How This Relates to Your Decision

So, Do You Really Need Identity Theft Protection in 2026?

Consider this comparison:

The question isn’t whether fraud happens.

It’s whether you want:

- To manage it alone

- Or to have structured monitoring and recovery assistance

Identity theft protection doesn’t eliminate risk.

But it can reduce detection time and recovery stress — which may significantly lower the true cost of an incident.

In the next section, we’ll examine who probably doesn’t need identity theft protection — because for some people, free tools and disciplined monitoring may be enough.

Who Probably Doesn’t Need Identity Theft Protection

Up to this point, we’ve examined how fraud happens and the real costs involved. But to honestly answer Do You Really Need Identity Theft Protection in 2026?, we also need to talk about the other side of the equation.

You may not need a paid service if you:

❌ Regularly monitor your credit reports

❌ Keep your credit frozen

❌ Actively track all financial activity

However, most people don’t maintain this level of monitoring consistently.

Let’s look at who might reasonably skip identity theft protection.

1️⃣ People Who Keep Their Credit Frozen at All Times

A credit freeze prevents lenders from accessing your credit report — which makes it extremely difficult for criminals to open new credit accounts in your name.

You can freeze your credit for free at:

- Experian

- Equifax

- TransUnion

The Consumer Financial Protection Bureau explains that a credit freeze is one of the strongest free defenses against new-account fraud.

If you rarely apply for credit and are comfortable temporarily unfreezing your report when needed, this alone blocks a major category of identity theft.

2️⃣ People Who Actively Monitor Their Financial Accounts Daily

If you:

- Check bank accounts daily

- Review credit card transactions regularly

- Use transaction alerts from your bank

- Pull your free credit reports periodically

You may already detect fraud quickly.

The Federal Trade Commission recommends frequent account review as a core fraud prevention habit.

If you’re disciplined and consistent, you may feel comfortable managing detection yourself.

3️⃣ Individuals With Minimal Digital Exposure

Risk often correlates with exposure.

You might be lower risk if you:

- Rarely shop online

- Avoid public WiFi

- Don’t store payment info on websites

- Limit social media usage

- Use strong unique passwords with two-factor authentication

The Cybersecurity and Infrastructure Security Agency outlines basic digital hygiene practices that significantly reduce risk.

If your online footprint is small and carefully managed, your exposure is naturally lower than average.

4️⃣ People Comfortable Handling Recovery Alone

If fraud happens, are you prepared to:

- File reports at IdentityTheft.gov

- Contact creditors directly

- Submit written disputes

- Monitor your credit long-term

The Federal Trade Commission provides step-by-step identity recovery instructions.

Some people prefer full control and are comfortable navigating bureaucracy independently.

If that’s you, identity theft protection may be less necessary.

5️⃣ Those With Strict Budget Constraints

Identity theft protection typically costs $10–$30 per month.

If you’re prioritizing:

- Paying down high-interest debt

- Building an emergency fund

- Covering essential expenses

It may be more financially responsible to use free safeguards first.

Free tools include:

- Credit freezes

- Bank transaction alerts

- Two-factor authentication

- Free credit reports

In some cases, the best financial move is strengthening fundamentals before adding subscriptions.

The Honest Bottom Line

So, Do You Really Need Identity Theft Protection in 2026?

You might not — if:

- Your credit is permanently frozen

- You actively monitor accounts

- Your digital exposure is limited

- You’re confident handling recovery alone

- Your budget is tight

However, many people underestimate their exposure or overestimate their ability to manage a fraud event under stress.

Identity theft protection isn’t mandatory.

It’s a convenience, monitoring expansion, and recovery support tool.

In the next section, we’ll look at who should strongly consider identity theft protection — because for certain groups, the risk profile changes significantly.

Who Absolutely Should Consider Identity Theft Protection in 2026

You should consider identity theft protection if you:

✔ Have multiple financial accounts

✔ Shop or bank online frequently

✔ Don’t regularly monitor your credit

✔ Want faster alerts and recovery support

If you don’t have time to track everything manually, a service can help simplify protection.

👉 See if Aura is right for your situation!

Here’s who should strongly consider it.

1️⃣ Families Managing Multiple Identities

The more Social Security numbers and financial accounts in a household, the larger the exposure.

Parents managing:

- Their own credit

- A spouse’s accounts

- Children’s SSNs

- Shared financial accounts

Face multiplied risk. If you’re comparing plans designed for households, see our complete guide to the Best Identity Theft Protection for Families.

Children are especially vulnerable to synthetic identity fraud because their credit files often go unchecked for years. The Federal Trade Commission warns that child identity theft can remain undetected until a teen applies for their first loan or job.

If you’re overseeing multiple identities, centralized monitoring and alerts may reduce blind spots.

2️⃣ Seniors and Retirees

Older adults are frequently targeted by fraud schemes, including:

- Social Security impersonation scams

- Medicare fraud

- Tech support scams

- Romance scams

We also created a dedicated guide to the Best Identity Theft Protection for Seniors if you’re comparing options for retirees.

The Federal Bureau of Investigation reports that older Americans consistently experience higher average fraud losses compared to younger age groups.

Many seniors also prefer assistance with paperwork and phone calls if fraud occurs — making identity restoration support particularly valuable.

For retirees on fixed incomes, quicker detection can be critical.

3️⃣ People Affected by Data Breaches

If your email, password, or SSN has been exposed in a breach, your long-term risk increases.

The Identity Theft Resource Center tracks thousands of breach incidents annually, affecting millions of consumers.

Even if no fraud has occurred yet, leaked credentials can circulate for years.

Monitoring services can alert you if exposed data resurfaces in new criminal marketplaces.

4️⃣ Frequent Online Shoppers and Digital Bankers

If you:

- Shop online weekly

- Use multiple payment apps

- Store credit cards on retail sites

- Bank primarily through mobile apps

Your exposure surface is larger than average.

According to cybersecurity guidance from the Cybersecurity and Infrastructure Security Agency, digital convenience increases risk when security hygiene isn’t perfect.

The more platforms you use, the more places your data lives.

Identity theft protection can add an additional monitoring layer beyond your bank’s fraud detection.

5️⃣ High-Income or High-Credit Individuals

If you have:

- Strong credit scores

- Large credit limits

- Investment accounts

- Business ownership

You can be an attractive fraud target.

Criminals often seek identities with high borrowing power.

Even short-term credit damage can impact mortgage rates or business financing.

For individuals with higher financial stakes, early alerts and guided recovery may justify the cost more easily.

6️⃣ Anyone Who Doesn’t Want to Handle Recovery Alone

Here’s a practical question:

If identity theft happened tomorrow, would you feel confident navigating:

- Credit bureau disputes

- Creditor fraud departments

- Legal documentation

- Extended monitoring afterward

The Consumer Financial Protection Bureau outlines formal dispute processes — but they can be time-consuming and stressful.

Some people simply prefer having professional assistance during complex financial problems.

And that preference alone can justify the subscription.

The Practical Conclusion

So, Do You Really Need Identity Theft Protection in 2026?

You should strongly consider it if:

- You manage multiple family members’ identities

- You are a senior or caring for one

- Your data has been exposed in a breach

- You conduct most of your finances online

- You have strong credit worth protecting

- You value recovery assistance during fraud events

Identity theft protection is not mandatory for everyone.

But for higher-risk groups, the combination of broader monitoring and recovery support can reduce both financial disruption and stress.

In the next section, we’ll evaluate whether the monthly cost is actually worth it — and how to decide logically rather than emotionally.

Is Identity Theft Protection Worth the Monthly Cost?

At this point, the real question becomes financial:

Do You Really Need Identity Theft Protection in 2026 — and is it worth paying for every month?

Most identity theft protection plans cost between $10 and $30 per month for individuals, and more for family coverage.

That’s roughly:

- $120–$360 per year (individual)

- $200–$500+ per year (family plans)

Whether it’s “worth it” depends on how you evaluate risk, time, and stress.

Let’s break it down logically.

1️⃣ Compare the Cost to Potential Fraud Losses

According to data published by the Federal Trade Commission, consumers report billions in fraud losses annually in the U.S.

While many credit card fraud cases are reimbursed, not all fraud is resolved instantly — and not all losses are fully covered.

Common non-reimbursed costs may include:

- Lost wages from time off work

- Legal documentation fees

- Notary and mailing expenses

- Temporary loss of access to funds

When evaluating cost, think in terms of risk transfer.

You’re not paying to prevent fraud entirely.

You’re paying for:

- Earlier detection

- Broader monitoring

- Guided recovery assistance

2️⃣ The Value of Time Saved

One of the most overlooked factors is time.

The Identity Theft Resource Center reports that recovery can take weeks or months depending on complexity.

Ask yourself:

- What is your time worth per hour?

- How many hours would you realistically spend fixing fraud?

- How stressful would the process be?

If a service assigns a recovery specialist to handle paperwork and disputes, that time savings has value.

For busy professionals or families, this alone may justify the monthly fee.

3️⃣ Your Personal Risk Profile Matters

The cost-benefit calculation changes depending on exposure.

Higher-risk profiles include:

- Frequent online shoppers

- Families managing multiple identities

- Seniors

- Individuals with high credit limits

- Anyone affected by prior data breaches

The Cybersecurity and Infrastructure Security Agency emphasizes layered security — meaning no single protection method is sufficient.

If your digital footprint is large, monitoring may provide meaningful added coverage.

4️⃣ Peace of Mind Has a Price

Not every financial decision is purely mathematical.

Some people are comfortable:

- Freezing their credit

- Monitoring accounts manually

- Handling disputes independently

Others prefer structured monitoring and knowing they’ll receive professional assistance if something goes wrong.

That peace of mind is subjective — but real.

5️⃣ When It’s Probably Worth It

Identity theft protection is more likely worth the cost if:

- You manage family members’ identities

- You don’t want to handle fraud recovery alone

- You’ve previously experienced identity theft

- You value centralized alerts instead of scattered bank notifications

- You prefer early warning beyond just credit report changes

For many households, the cost equates to a streaming subscription.

The question becomes:

Is proactive identity monitoring as important as entertainment?

6️⃣ When It May Not Be Worth It

It may not be worth the monthly fee if:

- Your credit is permanently frozen

- You actively monitor all financial accounts

- You have minimal digital exposure

- Budget constraints make subscriptions impractical

Free tools can provide strong baseline protection when used consistently.

Final Thought on Cost

So, Do You Really Need Identity Theft Protection in 2026?

For some, the answer is no — disciplined monitoring is enough.

For others, the relatively small monthly cost is a reasonable trade-off for:

- Broader detection

- Faster response

- Professional recovery assistance

- Reduced stress during fraud events

Identity theft protection is not a guarantee.

It’s a risk management tool.

In the next section, we’ll compare credit freezes directly with identity theft protection — and whether using both together offers stronger protection.

Credit Freeze vs Identity Theft Protection: Do You Need Both?

If you’re still deciding, Do You Really Need Identity Theft Protection in 2026?, this is one of the most important comparisons to understand.

Many people assume a credit freeze makes identity theft protection unnecessary.

That’s not entirely true.

A credit freeze is powerful — but it protects against a specific type of fraud.

Identity theft protection covers a broader range of risks.

Let’s break down the difference clearly.

What a Credit Freeze Actually Does

A credit freeze (also called a security freeze) prevents lenders from accessing your credit report.

If a criminal tries to open a new credit card or loan in your name, the lender typically cannot pull your credit file — and the application is denied.

You can place a freeze for free with:

- Experian

- Equifax

- TransUnion

The Consumer Financial Protection Bureau confirms that credit freezes are free and highly effective against new-account fraud.

This makes a credit freeze one of the strongest no-cost tools available.

What a Credit Freeze Does NOT Protect Against

Here’s where confusion happens.

A credit freeze does not protect against:

- Bank account takeovers

- Debit card fraud

- Tax refund fraud

- Medical identity theft

- Investment account fraud

- Data breaches

- Phishing scams

It only blocks new credit accounts from being opened through credit checks.

If someone drains your checking account or compromises your email, a freeze doesn’t help.

The Federal Trade Commission explains that identity theft includes many categories beyond credit-related fraud.

What Identity Theft Protection Adds

Identity theft protection typically includes:

- Credit monitoring

- Dark web monitoring

- Bank account monitoring

- Identity restoration specialists

- Insurance for eligible recovery expenses

Unlike a freeze, protection services monitor activity and alert you to suspicious behavior across multiple areas.

Some services also help with recovery if fraud occurs — something a freeze does not provide.

Should You Use Both?

In many cases, yes.

A credit freeze is free and highly effective against new credit fraud.

Identity theft protection may add:

- Broader detection beyond credit files

- Faster alerts across multiple accounts

- Professional recovery support

Think of it this way:

- A credit freeze = Preventive barrier against new credit accounts

- Identity theft protection = Monitoring and recovery system

They are not substitutes.

They address different risk categories.

When a Credit Freeze Alone May Be Enough

You may rely solely on a freeze if:

- You rarely apply for new credit

- You manually monitor bank and credit card accounts daily

- You’re comfortable handling recovery alone

- Your digital exposure is limited

For disciplined individuals, this layered self-management approach may work.

When Both Make Sense

Using both may be reasonable if:

- You manage multiple family members’ identities

- You have high credit limits

- You’ve been exposed in prior data breaches

- You prefer professional recovery support

- You want broader monitoring beyond just credit reports

The Cybersecurity and Infrastructure Security Agency recommends layered security practices — meaning multiple tools working together provide stronger protection.

The Bottom Line

So, Do You Really Need Identity Theft Protection in 2026 if you already froze your credit?

Maybe.

A credit freeze is an excellent first step.

But it only blocks one category of fraud.

Identity theft protection expands monitoring and may reduce recovery stress if something slips through.

For many people, the strongest setup is:

- Freeze your credit (free)

- Enable bank transaction alerts

- Practice strong password hygiene

- Add identity theft protection if broader monitoring and recovery support align with your risk tolerance

In the next section, we’ll look at the best identity theft protection options in 2026 and how they compare — so you can make a clear, confident decision.

Best Identity Theft Protection Options in 2026 (Quick Comparison)

If you’re trying to decide Do You Really Need Identity Theft Protection in 2026?, seeing how the top providers stack up side-by-side makes the decision clearer — especially if your goal is smart, practical protection and buyer intent.

Here’s a concise comparison of some of the most trusted identity theft protection services available in 2026, based on feature sets, monitoring capabilities, and value. For a deeper breakdown of features, pricing, and side-by-side rankings, see our complete guide to the Best Identity Theft Protection Services for 2026.

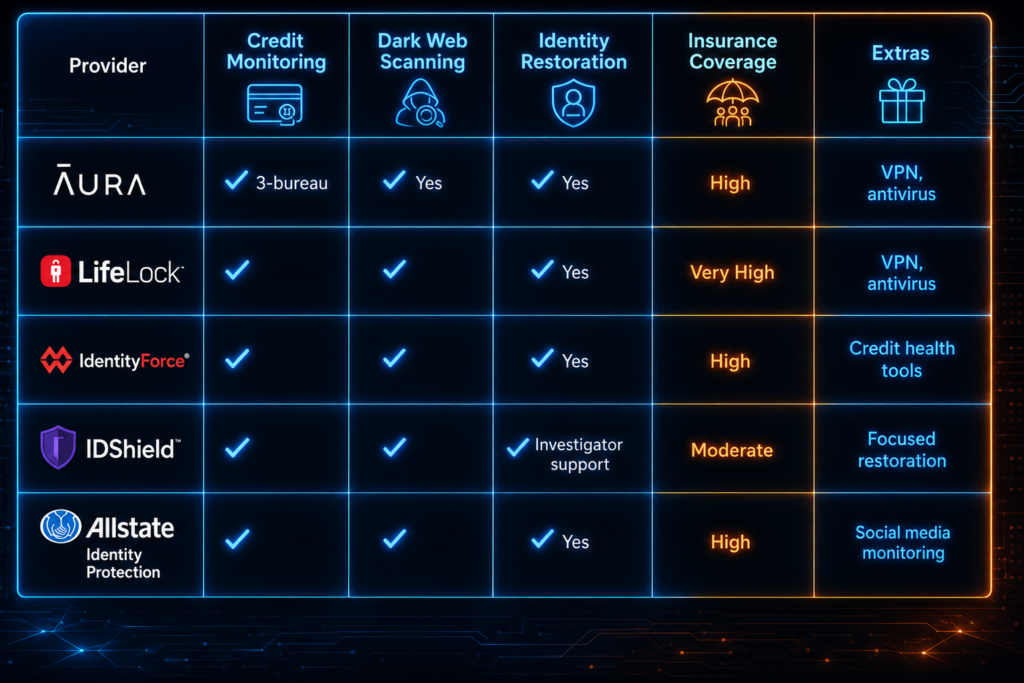

🔐 Aura – Best Overall Identity Theft Protection

Why it’s noteworthy:

Aura consistently ranks at or near the top in 2026 reviews, offering an all-in-one identity theft protection package that includes three-bureau credit monitoring, dark web scanning, identity restoration support, and extra cybersecurity tools like antivirus and VPN. If you want a detailed breakdown of its features, pricing, and real-world value, read our full review: Is Aura Worth It?

- Who it’s for: Individuals, couples, and families looking for comprehensive coverage

- Key perks: Broad monitoring, family plans, digital security extras

- Insurance: Up to several million depending on plan

- Best fit: People who want both identity and device protection in one place

🛡️ Norton LifeLock – Strong Protection with Premium Insurance

LifeLock is one of the most established names in identity theft protection. It offers solid dark web and credit monitoring, plus high-coverage insurance — especially useful for families or individuals with considerable financial exposure.

- Who it’s for: Those who value insurance depth and a trusted brand

- Key perks: Comprehensive identity monitoring + extras like antivirus/VPN in some plans

- Insurance: Up to $3M or more in eligible coverage

- Best fit: Families and high-risk users who want robust support

👨👩👧 IdentityForce – Comprehensive Financial Monitoring

IdentityForce is another respected provider that focuses strongly on financial monitoring alongside identity theft tools. It’s slightly more expensive but tailored for users who want detailed credit insights and restoration support.

- Who it’s for: Users focused on financial health and credit insights

- Key perks: Deep financial alerts, credit score reporting

- Insurance: Up to high-end coverage

- Best fit: People who want strong credit file intelligence

🧑💻 IDShield – Licensed Investigator Help

IDShield pairs standard identity theft protection with licensed investigator assistance — which is ideal if you want expert help during recovery. It doesn’t have the most advanced monitoring but offers support many users find valuable.

- Who it’s for: Those who want professional recovery assistance

- Key perks: Licensed investigators for restoration cases

- Insurance: Typically up to $1M+

- Best fit: People who want peace of mind with guided recovery

🧠 Allstate Identity Protection – Strong Coverage and Extras

Allstate Identity Protection earns high marks for its expansive monitoring (including social media) and generous insurance limits. It’s more feature-rich than basic plans and offers flexible pricing.

- Who it’s for: Users who want broad monitoring including social profiles

- Key perks: Multi-layer monitoring, high coverage limits

- Insurance: Often robust with family planning options

- Best fit: Users who want data filtering beyond financial accounts

Quick Side-by-Side Summary

👉 Services like Identity Guard also can help monitor your identity, track suspicious activity, and alert you to potential fraud before it becomes more serious.

Final Thoughts

So, Do You Really Need Identity Theft Protection in 2026?

If you want broader monitoring than free tools provide — including dark web scans, multiple credit bureau checks, and professional support if fraud happens — then yes, a paid service can be worth it.

Choosing the best identity theft protection depends on:

- Your risk profile

- Whether you want extra cybersecurity tools

- Your budget

- Whether you prefer guided recovery support

Services like Aura and LifeLock stand out for most users as a reliable blend of protection and buyer value. However, options like IdentityForce, IDShield, and Allstate are better fits for niche needs or focused coverage.

In the next section, we’ll help you make a confident decision based on your personal priorities — because understanding your own risk is just as important as choosing the right plan.

Final Verdict: Do You Really Need Identity Theft Protection?

You don’t have to pay for identity theft protection — but for most people, it’s worth it.

Monitoring everything manually takes time, and it’s easy to miss early warning signs.

Identity theft protection services provide continuous monitoring, real-time alerts, and recovery support — which can help reduce the risk of serious financial damage.

If you want a simple, all-in-one solution, Aura is the best choice for most people.

👉 Start protecting yourself with Aura here!

📊 The Core Decision Factors

To decide whether identity theft protection is worth it for you, ask yourself the following:

- What is your risk exposure?

Do you shop online frequently? Manage multiple accounts? Have a large digital footprint? - How comfortable are you handling fraud recovery on your own?

Would you prefer expert help if something goes wrong? - What is your tolerance for uncertainty?

Some people value peace of mind over chasing alerts manually. - Does the monthly cost fit your budget?

Evaluate identity theft protection like insurance — you pay to reduce risk and stress.

External resource: The Federal Trade Commission offers helpful guidance on fraud prevention and recovery if you want to explore free alternatives.

🟩 When You Probably Do Need Protection

Identity theft protection in 2026 likely makes sense if:

✔ You manage multiple family members’ identities

✔ You’ve been part of a data breach

✔ You bank and shop online frequently

✔ You want early alerts beyond free credit checking

✔ You value recovery support and guided resolution

In these scenarios, identity protection serves as both an early warning system and a recovery assistant — which can be especially valuable when time and accuracy matter.

🟥 When You Might Not Need Protection

In contrast, you may feel comfortable without paid protection if:

✔ You keep your credit frozen at all times

✔ You actively monitor accounts daily

✔ You have minimal online exposure

✔ You are comfortable with DIY recovery processes

✔ Free tools fit your risk tolerance and budget

Placing a credit freeze and using free account alerts can cover many basic fraud scenarios.

External resource: The Consumer Financial Protection Bureau offers step-by-step instructions for freezes and disputes if you choose the DIY route.

💡 How Identity Theft Protection Fits Into Your Overall Security

Rather than seeing identity theft protection as an either-or, it’s more useful to think of it as part of a layered security plan — similar to antivirus software, firewalls, and strong password habits.

Here’s how it fits:

🔹 Credit freeze: Blocks new credit from being opened in your name

🔹 Free credit monitoring: Tracks credit report changes

🔹 Identity theft protection: Monitors a wider range of data sources and provides professional support

🔹 Strong habits: Unique passwords, two-factor authentication, cautious online behavior

Together, these layers reduce risk more effectively than any single tool.

📉 The Emotional Component

One thing that often gets overlooked is stress.

The Identity Theft Resource Center reports that the emotional impact of identity theft can linger long after the financial issues are resolved.

If having expert support reduces that stress — even at a monthly cost — that peace of mind may be worth it for many.

🧠 Bottom Line

So… Do You Really Need Identity Theft Protection in 2026?

Yes — if:

- You’re at moderate to high risk

- You want early, broader detection

- You value dedicated support

- You want to simplify fraud resolution

Not necessarily — if:

- You effectively use free protections

- You’re confident handling fraud recovery

- You manage a low digital risk profile

- The cost feels unnecessary based on your situation

Identity theft protection doesn’t guarantee prevention — but it does offer enhanced monitoring and support that free tools alone can’t fully replicate.

Ultimately, the right choice depends on how much risk, time, and stress you’re willing to manage on your own versus transferring some of that burden to specialists.

When you weigh both risk and convenience in 2026’s digital landscape, identity theft protection can be a practical investment — especially for those who want broader security and guided peace of mind.

If you’re ready, the next section will help you choose the right plan based on your specific needs and budget.

Frequently Asked Questions About Identity Theft Protection in 2026

If you’re still wondering, Do You Really Need Identity Theft Protection in 2026?, these common questions will help you make a clear and confident decision.

This section is designed to address the exact concerns most buyers have before signing up.

1️⃣ Can Identity Theft Protection Actually Prevent Fraud?

No service can prevent all fraud.

Identity theft protection is designed to:

- Monitor your personal information

- Alert you to suspicious activity

- Provide recovery assistance if fraud occurs

It reduces detection time and simplifies recovery — but it does not eliminate risk entirely.

The Federal Trade Commission explains that fraud prevention always requires layered security and consumer awareness.

2️⃣ Is Identity Theft Protection the Same as Credit Monitoring?

No.

Credit monitoring only tracks changes to your credit report.

Identity theft protection may include:

- Dark web monitoring

- Bank account monitoring

- Identity restoration specialists

- Insurance for eligible recovery expenses

If you only use free credit monitoring, you may miss fraud that doesn’t impact your credit file.

3️⃣ If I Freeze My Credit, Do I Still Need Identity Theft Protection?

A credit freeze is a strong free tool.

However, it only blocks new credit accounts from being opened.

It does not protect against:

- Bank account takeovers

- Phishing scams

- Tax refund fraud

- Medical identity theft

The Consumer Financial Protection Bureau explains that a freeze prevents new credit but doesn’t cover other identity theft categories.

Some people use both for layered protection.

4️⃣ How Much Does Identity Theft Protection Cost in 2026?

Most plans range from:

- $10–$30 per month for individuals

- Higher for family plans

The real question isn’t just price.

It’s whether the monitoring, alerts, and recovery support justify that cost for your risk profile.

If you’re asking Do You Really Need Identity Theft Protection in 2026?, compare the monthly fee to the time and stress you’d face handling fraud alone.

5️⃣ What Happens If My Identity Is Stolen Without Protection?

You can still recover.

The Federal Trade Commission provides free step-by-step recovery guidance at IdentityTheft.gov.

However, you’ll be responsible for:

- Contacting creditors

- Filing disputes

- Monitoring accounts

- Tracking documentation

Paid services may assign a specialist to help manage this process.

6️⃣ Is Identity Theft Protection Worth It for Families?

Families often face increased exposure because:

- Multiple Social Security numbers are involved

- Children’s credit files are rarely monitored

- Shared financial accounts create wider risk

The Identity Theft Resource Center notes that child identity theft can go undetected for years.

For households managing several identities, centralized monitoring may provide additional value.

7️⃣ Does Identity Theft Protection Improve My Credit Score?

No.

Identity theft protection does not directly increase your credit score.

However, early detection of fraudulent activity can prevent long-term credit damage — which indirectly protects your score.

Monitoring helps maintain credit health, but it doesn’t build credit.

8️⃣ How Do I Choose the Best Identity Theft Protection Service?

When comparing providers, consider:

- One vs three-bureau credit monitoring

- Dark web monitoring coverage

- Identity restoration support

- Insurance limits

- Family plan options

- Extra cybersecurity tools (NordVPN, antivirus, password manager)

Focus on features that align with your risk profile rather than just the lowest price.

Final FAQ Takeaway

If you’ve read this far, you likely have a serious interest in protecting your personal data.

So, Do You Really Need Identity Theft Protection in 2026?

If you:

- Want broader monitoring beyond free tools

- Prefer guided recovery support

- Manage multiple identities

- Have significant digital exposure

Then identity theft protection can be a rational investment — not just a marketing upsell.

If you’re disciplined with free safeguards and comfortable handling disputes independently, you may decide it’s optional.

The key is making a decision based on facts — not fear.

Now that you understand the risks, costs, and options, you can choose the level of protection that matches your financial and digital reality in 2026.

Pingback: Aura vs Identity Guard: Which Identity Theft Protection Is Better in 2026? - Riich Niich

Pingback: LifeLock vs Identity Guard: Which Identity Protection Service Is Better in 2026? - Riich Niich

Pingback: Is Aura Better Than Free Credit Monitoring? - Riich Niich

Pingback: Best Password Managers (2026 Guide): Protect Your Accounts From Hackers - Riich Niich

Pingback: Aura vs Experian IdentityWorks: Which Identity Protection Service Is Better in 2026? - Riich Niich

Pingback: Best Antivirus for Families (2026 Guide) - Riich Niich

Pingback: 13 Warning Signs Someone Stole Your Identity (And What To Do Immediately) - Riich Niich

Pingback: How Identity Theft Happens (Most People Don’t Know This) - Riich Niich

Pingback: NordProtect Review (Is It Really Worth It in 2026?) - Riich Niich

Pingback: How Hackers Get Your Personal Data (And How to Stop Them) - Riich Niich

Pingback: How to Remove Your Personal Information from the Internet (2026 Guide) - Riich Niich

Pingback: NordVPN vs Surfshark: Which VPN Is Better in 2026? - Riich Niich

Pingback: Public WiFi Dangers (And How To Stay Safe) - Riich Niich

Pingback: Is Incogni Worth It in 2026? (Full Review + Results) - Riich Niich

Pingback: Is Surfshark Worth It? Full Review, Pros, Cons & Real Value - Riich Niich

Pingback: How to Protect Yourself from Identity Theft (Step-by-Step Guide) - Riich Niich

Pingback: Why Insider Threats Are More Dangerous Than Hackers (Real Risks Explained) - Riich Niich

Pingback: Identity Monitoring vs Credit Monitoring: What's the Difference? (2026 Guide) - Riich Niich